Free Consultation. Free Finance Assessment. No Obligation.

At Willow Private Finance, there isno charge to speak to one of our specialist advisorsandno charge for us to assess your requirements and identify suitable finance solutions.

We'll take the time to understand your circumstances, review your objectives and explore the options available to you before you decide whether you want to proceed.

Should you wish to move forward with a recommended solution,any applicable fees will be clearly explained and agreed in advance, ensuring complete transparency from the outset.

Once instructed, we'll manage the process from application through to completion, liaising with lenders, solicitors, valuers and other professionals involved in the transaction to help secure the funding you require.

Mortgage to Build Home: Your UK Self-Build Guide 2026

You may already have the plot under offer, planning drawings in progress, and a builder lined up, yet the finance still feels like the least transparent part of the entire project.

That is normal. A mortgage to build home is not a standard residential mortgage with a different label. It is a specialist funding structure built around construction risk, valuation risk, timing risk, and lender control. The key challenge is not merely getting a yes. The challenge is arranging a facility that matches how the build will move on site.

For straightforward cases, that means choosing the right stage-payment product and preparing the application properly. For more complex cases, it can mean combining land finance, self-build funding, bridging, development finance, or private bank liquidity in a way that protects cash flow and keeps the project moving if one part of the plan changes.

From Grand Designs to Financial Foundations

Most borrowers begin with the house they want to create. Lenders begin with what could go wrong before that house exists.

That difference in perspective matters. A standard mortgage is secured against a completed property with an established market value. A self-build mortgage is secured against a project that has to be delivered in stages, checked repeatedly, and funded in a controlled sequence. The underwriting is therefore broader. It looks at the borrower, but also the land, the planning position, the build method, the contractor strategy, and how realistic the budget is.

Why self-build finance feels harder than it should

Many capable borrowers assume this type of lending is inaccessible because the market is opaque. That view is understandable. There is a recognised information gap around construction-to-permanent borrowing in the UK, particularly for first-time builders, with little clear public guidance on how lenders structure these facilities or how affordability rules are applied in practice.

The practical result is that borrowers often approach the process with the wrong assumptions. They expect one application, one valuation, one completion date, and one release of funds. Self-build lending does not work like that.

The primary issue is usually presentation, not possibility

In many cases, lender appetite exists. What fails is the way the case is packaged.

Underwriters want evidence that the project has been thought through with professional discipline. That means coherent plans, a build cost schedule that stands up to scrutiny, sensible sequencing, and a borrower who understands where cash will be needed before the next tranche arrives.

Key takeaway: A self-build mortgage is less about convincing a lender that your home design is exciting, and more about proving the project can be delivered without funding stress.

For well-informed borrowers, this becomes a structuring exercise rather than an application. A high-net-worth client may have excellent balance sheet strength but still choose the wrong product if they need flexibility during the build. A developer moving into a one-off bespoke residence may underestimate how differently lenders treat a personal home compared with a profit-led scheme. A borrower pursuing modular or sustainable construction may discover that two lenders view the same specification in very different ways.

The strongest cases are organised like professional project files, not aspirational mood boards. That is the shift that turns a difficult process into a manageable one.

Choosing the Right Construction Finance Structure

The first decision is not which lender to call. It is how the money needs to arrive.

Self-build finance usually works on a stage payment basis. The key distinction is whether those payments are made in arrears or in advance. The wrong choice can leave an otherwise well-funded project short of working cash at exactly the wrong moment.

Arrears stage payments

This is the more familiar structure. The lender releases funds after a construction stage has been completed and inspected.

That gives the lender more control because value has already been created before further money is advanced. It also means the borrower must bridge each stage with their own capital, contractor credit, or another source of liquidity.

Arrears can work well if you have:

Strong available cash: You can pay for groundworks, shell costs, and interim invoices before reimbursement.

Predictable contractor terms: Your builder is not demanding aggressive payment timing.

A conservative project plan: You are content with a slower, inspection-led release process.

The problem appears when the build is perfectly viable overall but the cash flow between milestones is too tight. That is where borrowers start paying for delays they did not budget for.

Advance stage payments

An advance stage payment mortgage releases funds before the stage begins. Fewer lenders offer this, and the underwriting is often more selective.

For the borrower, the advantage is obvious. Cash reaches the project before invoices fall due, which eases strain during the most capital-intensive stages.

Advance structures can suit:

Borrowers with good net worth but limited desire to tie up liquidity

Projects with fast-moving contractor schedules

Complex builds where holding extra cash outside the project is strategically useful

The trade-off is that lenders taking this approach are relying more heavily on the initial appraisal, the project documents, and the credibility of the team around the build.

A useful point of comparison with larger schemes can be seen in specialist thinking around development finance, where drawdowns, monitoring, and build viability are assessed through a similarly structured risk lens.

Contract strategy also affects lender comfort

The finance structure and the build contract are linked. Lenders tend to prefer certainty where they can get it.

A fixed-price contract can make the funding case cleaner because the build cost is easier to defend. A cost-plus arrangement may offer flexibility on design and procurement, but it can make underwriters more cautious if there is no firm cap on final expenditure.

That does not mean cost-plus is unfinanceable. It means the surrounding documents must be tighter. If the borrower is retaining more control over procurement and package management, the lender will usually want clearer evidence that cost discipline is still in place.

What works and what does not

A simple rule is worth keeping in mind.

What works: Matching the mortgage structure to the build’s actual cash cycle.

What does not: Choosing the cheapest-looking product without testing whether the timing of releases is workable.

A borrower can be asset-rich and still create a problem by selecting arrears funding for a project that really needs advance liquidity. Equally, a borrower can pay a premium for advance funding they do not need if they already have sufficient capital on hand.

The right answer is rarely abstract. It sits in the detail of the programme, the contractor payment schedule, and the borrower’s wider liquidity strategy.

Meeting Lender Eligibility and Deposit Criteria

A self-build case can look strong on income and still fail at underwriting because the land title is messy, the specification is too thin, or the borrower has no clear plan for funding overruns. Lenders assess the project as a finance structure, not just as a mortgage application.

In practice, I look at four points first: the plot, the technical pack, the cost base, and the borrower’s liquidity. If one of those is weak, the pricing, loan-to-value, and lender choice usually narrow fast.

The plot

The site underpins the whole proposal. If the land cannot be valued cleanly, serviced properly, or sold in a reasonable market if things go wrong, lender appetite drops.

Planning status matters, but so does legal and practical usability. Access rights, restrictive covenants, drainage, utilities, contamination risk, slope, and unusual location issues can all affect whether a lender will proceed and on what terms. A plot with full planning but awkward access can be harder to finance than a cleaner site with fewer complications.

Borrowers still acquiring land need to structure this carefully. The route for plot purchase, refinance of an already-owned site, and combined land-and-build funding are not the same. The funding options set out in this guide to using a mortgage for land purchases in the UK are often the starting point, because the land position shapes the rest of the case.

The plans

Underwriters back documented projects, not concepts.

A lender will usually want detailed drawings, planning documentation, build specifications, a realistic programme, and a clear route to warranty sign-off and building regulations approval. If the design is bespoke, the paper file has to do more work. It needs to show that the project is buildable, insurable, and likely to produce a marketable end asset.

That becomes more important with architect-led schemes, basement builds, listed or sensitive sites, and homes using unfamiliar materials or methods.

Non-standard and sustainable construction

Non-standard does not mean unacceptable. It means the lender and valuer need a clearer explanation of risk.

Timber frame, SIPs, ICF, modular construction, and heavily sustainability-led designs can all be financeable, but not across the whole lender market. Some institutions are comfortable where there is an established manufacturer, recognised certification, and a sensible resale profile. Others will decline early because the valuer may struggle to support the end value or because the credit policy is written around conventional brick-and-block housing. The practical result is the same. Product choice becomes a lender appetite exercise, not a rate-shopping exercise.

That is where specialist placement matters. For higher-value projects or unusual designs, the job is often less about finding a lender that says yes in principle and more about finding one whose credit team, valuer panel, and policy all line up.

The costs

Weak cost control is one of the quickest ways to damage credibility.

The budget needs to be detailed enough for an underwriter and valuer to test it against the plans and local build realities. Broad assumptions rarely survive scrutiny, especially where abnormal ground conditions, retaining works, specialist glazing, renewable systems, or complex engineering are involved. If the cost schedule looks light, the lender will assume further capital will be needed later and will question whether the borrower can supply it.

A strong file usually shows:

Build costs by trade or package: Groundworks, structure, roof, windows, M&E, internal finishes, external works.

Professional and statutory costs: Architect, engineer, project manager, warranty provider, planning conditions, building control, and certification.

Site-specific expenditure: Service connections, access works, drainage, retaining structures, remediation, and any other abnormal items.

Contingency funding: A stated reserve that reflects the build complexity, rather than an optimistic assumption that nothing will slip.

For experienced clients, I also want to know where that contingency sits. Held in cash personally, retained inside a wider facility, or dependent on selling another asset are three very different risk profiles.

The borrower

Income still matters, but self-build lenders also assess resilience.

They want to see that the borrower can service the debt during the build, withstand delays, and inject funds where required without destabilising their wider position. For employed borrowers this may be straightforward. For company owners, fund managers, partners, entrepreneurs, and clients drawing mixed income from salary, dividends, trust distributions, carried interest, or bonus structures, the case needs to be presented properly from the outset.

Deposit and equity are just as important. More equity usually improves terms, but the headline percentage is only part of the story. Lenders also look at where that equity sits. In the land, in cash, or in another asset that still needs to be sold. A borrower who owns an unencumbered plot may be in a stronger position than someone with a larger cash deposit but no site security. Equally, a borrower with substantial net worth can still run into friction if their liquidity is tied up in illiquid holdings or tax-sensitive structures.

The same principle applies to credit profile and account conduct. Historic issues do not always kill a case. Unexplained borrowing, fresh commitments, or inconsistent bank activity during underwriting often create more concern than an older, well-documented event.

For high-net-worth clients and experienced developers, the discussion is rarely limited to eligibility. The better question is how the facility should be structured so the project remains financeable if costs rise, timings slip, or the completed property needs to be refinanced onto a different basis. That may mean using a self-build mortgage, a private bank facility, short-term development finance, or a blended structure that protects liquidity while keeping lender conditions workable.

Related Guide

Self-Build Projects Often Require More Than A Standard Mortgage

As this guide demonstrates, financing a self-build is about far more than borrowing against a completed property. Stage payments, cash flow management, land acquisition, build costs and lender appetite all influence whether a project progresses smoothly or encounters unnecessary delays. For larger or more complex builds, the right funding structure can be just as important as the design itself.

Our Complex Property Finance Guide explains how specialist funding solutions, including self-build finance, development funding, bridging loans and private banking facilities, can be combined to support ambitious construction projects while protecting liquidity and providing the flexibility needed as your build evolves.

A client reaches shell stage, the contractor wants paying on Friday, and the lender’s valuer cannot inspect until Tuesday. That four-day gap is how otherwise well-funded self-builds run into pressure.

Drawdown is where finance structure stops being theoretical. It becomes a live cash management exercise, shaped by inspection timing, lender interpretation of stage completion, contractor payment terms, and the borrower’s ability to cover short gaps without distorting the wider plan.

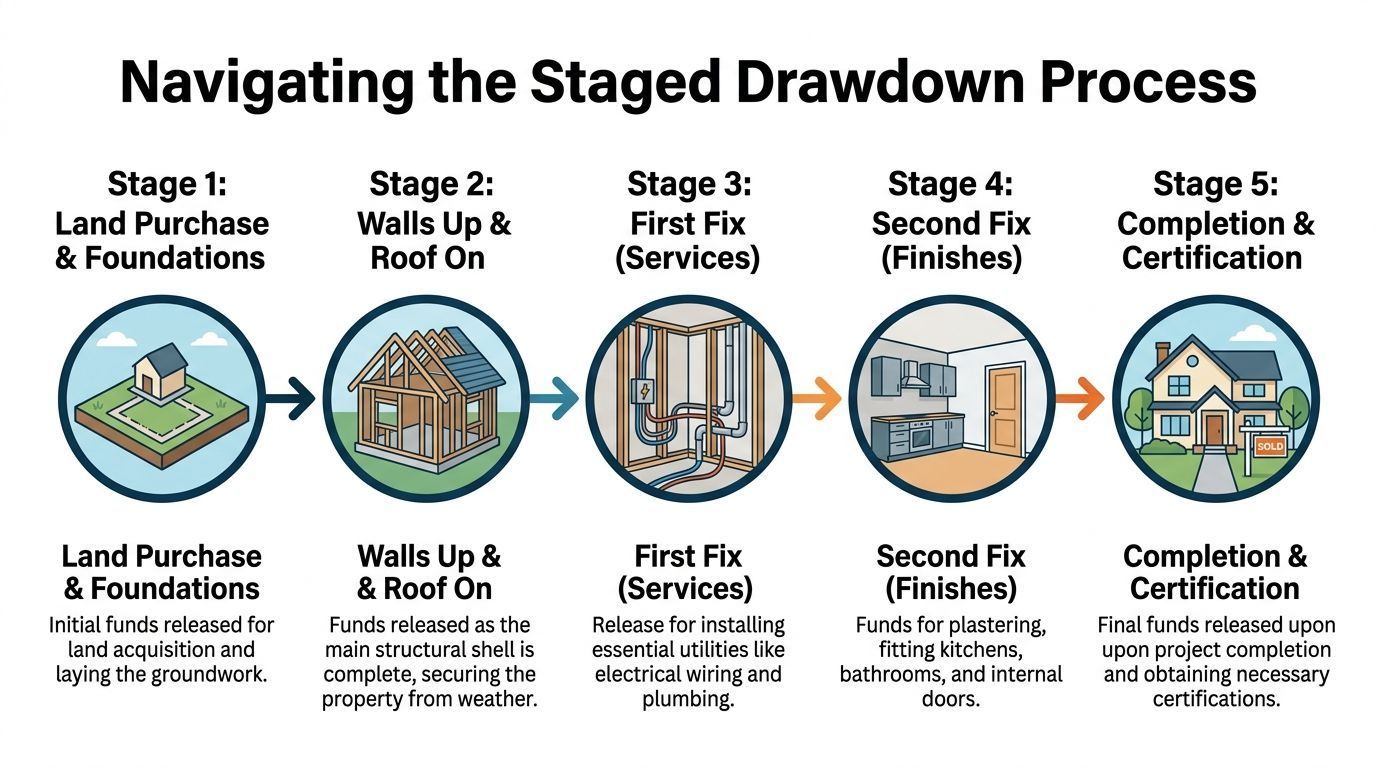

How stage releases usually work

Lenders release funds in tranches as the site progresses and value is created. The names vary by lender, but the pattern is broadly consistent:

Land purchase or initial release This can fund the plot purchase, refinance land already owned, or provide the agreed opening tranche.

Foundations Groundworks are completed, then inspected before the next release is considered.

Structure to shell stage The frame, walls, and roof are sufficiently advanced for the property to have clear form and measurable value.

Wind and watertight The external envelope is substantially complete, allowing internal works to proceed.

First fix Plumbing, electrics, and other core services are installed.

Second fix and finishes Joinery, kitchens, bathrooms, plastering, and fittings move the project towards completion.

Final sign-off The last tranche is released once the lender has the completion evidence and certificates it requires.

The strategic point is not the list itself. It is whether the stage definitions in the offer match the way your contractor, quantity surveyor, and project manager will deliver the build. On more complex projects, especially split contracts, bespoke design-and-build arrangements, or larger sites built in phases, lenders can monitor progress far more closely. Borrowers handling those structures should understand how lenders assess multi-stage and phased development finance, because the same control logic often applies even on a single prime residence.

The surveyor often controls the pace

Many borrowers focus on the lender relationship and underestimate the monitoring surveyor.

That is risky.

The surveyor decides whether a stage has been achieved in a way the lender can fund. A contractor may regard the works as practically complete for that phase. The valuer may still see missing items, incomplete certification, or insufficient value added to support the release. In a standard case that creates delay. In a high-spec or non-standard build, it can create a material funding mismatch if the lender is already cautious on final value or build method.

The cleaner approach is to manage inspections proactively. Book them early. Make sure the site is ready. Check that invoices, stage certificates, and contractor statements line up with the milestone being claimed.

Cash flow needs to be modelled before the first invoice lands

A self-build mortgage is only one source of site liquidity. It should not be treated as a tap that turns on exactly when the contractor asks.

Before works start, the borrower and broker should know:

Which costs must be paid before a stage can be certified

How long the lender usually takes from inspection to release

Whether the contractor will continue through a short payment gap

What reserve cash is available if the release is lower than expected

Which professional fees and VAT items fall outside the lender's stage logic

This matters even more for affluent clients who could cover a shortfall but would rather not pull liquidity out of an investment portfolio, trust structure, or business at the wrong moment. Good structuring protects optionality. It avoids forced asset sales, expensive short-term borrowing, and avoidable friction with tax planning.

Expert point: Model the drawdown schedule against the contractor payment calendar line by line. If those two documents tell different stories, the pressure point will show up during the build, not on the spreadsheet.

Low interim valuations create funding gaps

One of the quieter risks in self-build finance is an inspection that supports less value than expected at a given stage.

If that happens, the lender may reduce or delay the tranche. The shortfall usually has to be covered from cash, a separate facility, or a revised build sequence. For straightforward projects, that can be inconvenient. For architect-designed homes, MMC schemes, listed conversions, or builds with unusually high specification early in the programme, it can become a structural issue because spend and lender-recognised value do not always rise in step.

In these cases, specialist broking earns its place. The case should be placed with a lender whose valuer base, policy, and appetite suit the asset class from day one, rather than hoping a mainstream stage model will adapt later.

Paperwork quality changes outcomes

Drawdown delays are often administrative before they are financial.

Missing invoices, unsigned certificates, inconsistent build cost schedules, and unclear evidence of stage completion all slow releases. Retentions can also catch borrowers out. Some lenders hold back part of the final advance until completion formalities are fully satisfied, so the last stretch of the build needs its own cash plan.

Well-run projects keep a disciplined file from the start. That means current costings, clean contractor documentation, accessible warranties and certificates, and a clear chain of responsibility for who submits what to the lender and when.

The smoother the file, the smoother the money.

Managing Costs Timelines and Inevitable Risks

Six months into a self-build, the pressure rarely comes from a single dramatic problem. It usually starts with a small cost increase, then a variation signed too casually, then a contractor payment requested earlier than planned, then a programme slip that pushes inspections, professional fees, and interim living costs wider than the original cash model allowed.

That sequence matters because self-build finance is not forgiving when time and cost drift at the same time.

Cost overruns need to be structured into the funding plan

The application budget is a working model. It is not the final truth of the build.

On straightforward schemes, that may only mean a larger contingency. On higher-value homes, complex refurbishments, basement works, listed assets, or non-standard construction, the issue is more strategic. Early-stage spend can run ahead of lender-recognised value. Imported materials can move on lead time and price. Specification decisions made late can absorb cash that was meant to protect the programme.

Clients with strong balance sheets still get caught here if they commit too much liquidity too early. A better structure is to separate core build cost, contingency, and reserve liquidity from the outset, then decide which pot is available for overruns and which pot is being protected for lender timing, retention release, or refinance risk.

Borrowers dealing with margin pressure should also understand how build cost inflation affects LTC calculations, because lender comfort can tighten even where the project remains affordable on paper.

Delays change the finance profile of the project

A delayed build is not just an inconvenience.

It can increase interest, extend rent or bridging costs, push out redemption dates, and create pressure if the original facility assumed completion within a set term. For HNW borrowers and developer-style clients, this is often where the distinction between available wealth and available liquidity becomes important. An asset-rich client can still face a poor funding position if capital is tied up elsewhere and the build needs more time than the lender originally expected.

The right response starts before work begins. Programme assumptions should be realistic, not flattering. Contracts should deal properly with extensions of time, variations, and payment triggers. The professional team should know who is responsible for reporting delays to the lender before they become a covenant or term issue.

Contractor weakness can become a funding event

Poor contractor selection is one of the fastest ways to destabilise a build.

Price matters, but contractor resilience matters more. The finance plan depends on the builder's ability to hold programme, manage subcontractors, control variations, and issue paperwork that stands up to lender scrutiny. A contractor who is cheap at tender stage can become expensive very quickly if cash flow is weak, supervision is thin, or procurement is unreliable.

For larger or more bespoke projects, I would expect proper diligence before appointment:

Recent client references, preferably from projects of similar size and complexity

Current insurance evidence, checked against the actual scope of works

A clear payment schedule, tied to progress rather than front-loaded deposits

Variation control, with written pricing and approval before works proceed

Visibility on subcontractors and procurement, especially where specialist trades or long-lead items are involved

If a builder resists that level of transparency, the concern is not only construction quality. It is whether the funding structure is being exposed to avoidable execution risk.

Control comes from cash discipline and decision discipline

The clients who finish well tend to do three things consistently.

They keep reserve liquidity rather than using every pound at the start. They monitor actual spend against the cost plan every month, not only when the lender asks for evidence. They escalate issues early, with the contractor, quantity surveyor, architect, and broker involved before a problem hardens into a missed deadline or a funding gap.

That matters even more on projects with bespoke design, accelerated timelines, or unusual construction methods, because lender appetite can narrow quickly once a scheme starts to look less like the original proposal.

A mortgage to build home successfully is not just about securing approval at the start. It is about keeping the finance structure credible all the way to completion, with enough cash, enough reporting discipline, and enough flexibility to absorb the problems that almost every build encounters.

Advanced Strategies and Finance Alternatives

A client secures a rare plot on Friday, exchanges are required by Tuesday, and the design includes a basement, extensive glazing, and a mix of modern methods of construction. A standard self-build mortgage may still play a role, but it is rarely the right first facility in a case like that. The finance needs to be structured around speed, planning risk, build complexity, and the exit route from day one.

That is the point experienced borrowers and their advisers often miss. The question is not which product funds a build. The question is which structure gives the project the best chance of reaching completion without a late-stage refinance problem, a cash squeeze, or a lender withdrawing appetite once the build departs from the original narrative.

When bridging makes more sense

Bridging suits transactions where timing matters more than long-term pricing.

That usually means one of three things. The plot has to complete quickly. Planning enhancement or early works need to happen before a mainstream lender will engage. Or the borrower wants to separate land acquisition from the longer-term build facility to keep options open.

Used well, bridging buys control. Used badly, it magnifies pressure.

The discipline is in the exit. Before drawdown, the borrower should already know whether the refinance is likely to be onto a self-build mortgage, a term mortgage on completion, or a sale. The mechanics of bridging to mortgage transitions should be understood at the outset, because the wrong title structure, planning condition, build method, or valuation assumption can make the refinance harder than expected.

When development finance is the better fit

Development finance is often the better structure where the project starts to look like a scheme rather than a home build.

That can include multi-unit sites, heavier refurbishment with ground-up elements, borrower SPVs, profit-led exits, or projects where lender underwriting needs to focus on gross development value, cost-to-complete, contractor strength, and sales risk. In those cases, trying to force the deal into an owner-occupier self-build product can create unnecessary friction.

The trade-off is tighter control. Expect detailed due diligence, monitoring surveyors, staged releases against verified progress, and closer scrutiny of contingencies and professional team quality. For experienced developers, that can be entirely workable. For private clients building one complex residence, it can still be the right answer if the design, programme, or exit profile sits outside mainstream mortgage appetite.

In practice, lender appetite turns on presentation as much as headline wealth. A professionally assembled pack, with planning history, build contract position, cost plan, cashflow, and clear exit analysis, will usually open more doors than a loosely framed proposal with strong assets behind it.

When private bank or securities-backed borrowing is worth considering

For high-net-worth clients, the best structure is often the one that preserves flexibility elsewhere.

A private bank may lend against the wider balance sheet rather than treating the project as a standalone retail mortgage case. That can suit borrowers with concentrated liquidity events pending, investment portfolios they do not want to liquidate, trust ownership, cross-border income, or a desire to avoid repeated reimbursement stages where cash is available but operational simplicity matters more.

That does not make private banking automatically cheaper. It can be more efficient in the right hands, but the pricing, security package, and covenants need close review. Securities-backed borrowing also introduces a different risk profile. If markets move against pledged assets, the borrower may face calls for additional collateral at exactly the wrong point in the build cycle.

Trigger points that justify an alternative route

A standard mortgage to build home often stops being the obvious answer where one or more of these factors is present:

The acquisition timetable is too short for mainstream underwriting

The construction method, specification, or design narrows lender appetite

The project is held in a company, trust, or wider wealth structure

The site has multiple units or a commercial exit

The borrower wants maximum liquidity efficiency, not just maximizing financial gearing. The refinance relies on

The refinance relies on planning progression, practical completion, or a future sale

The common thread is strategic fit. Good structuring matches the facility to the actual risk in the project, not to the label the borrower started with.

In complex cases, a specialist broker does more than source rates. The broker tests lender appetite before application costs are incurred, frames the case for the right credit audience, and sequences the facilities so the exit from one product is credible before the first one begins. That is often the difference between a finance plan that looks workable on paper and one that remains workable when the project becomes more expensive, slower, or less standard than first expected.

Tailored advice for individuals, businesses and professional advisers seeking sophisticated financial solutions.

At Willow Private Finance, we understand that every client has different ambitions, financial circumstances and long-term objectives. Whether you are purchasing property, refinancing existing borrowing, protecting your family or business, or looking to unlock wealth through specialist lending, we build solutions around your individual needs rather than forcing you into standard products.

As an independent, whole-of-market brokerage, we provide access to residential mortgages, buy-to-let finance, bridging loans, development finance, commercial lending, private banking and Lombard lending facilities, alongside a comprehensive range of personal and business protection solutions. Our expertise extends to UK and international clients, high-net-worth individuals, company directors, investors, expatriates and borrowers with complex financial structures.

By combining deep technical expertise with relationships across mainstream lenders, specialist lenders and private banks, we help clients secure funding, structure borrowing efficiently and protect the assets, income and people that matter most. Whatever stage of your financial journey you are at, our team is here to provide clear, strategic advice that delivers confidence and long-term value.

From mortgages and private banking to Lombard lending, business finance and protection planning, Willow Private Finance delivers bespoke solutions for even the most complex financial requirements.

Wesley Ranger is a senior finance professional with over 20 years’ experience in the UK mortgage and specialist lending markets. As a director at Willow Private Finance, he has extensive experience advising on self-build and construction finance across a range of project types.

His expertise includes structuring staged funding facilities, navigating lender criteria for plot purchase and build phases, and assessing risk in projects involving contractors, architects, and phased development. Wesley has worked with both first-time self-builders and experienced developers to structure funding aligned with build timelines and lender requirements.

He has a detailed understanding of how lenders assess self-build projects, including cost viability, contingency planning, and borrower experience. His experience spans both high street and specialist lenders, providing a comprehensive, whole-of-market perspective on construction finance.

Wesley regularly advises on structuring self-build projects to ensure that funding aligns with both construction milestones and long-term financial objectives.

Important Notice

This article is for general information purposes only and does not constitute personal financial advice, tax advice, or legal advice. Mortgage availability, criteria, and rates depend on individual circumstances and may change at any time.

Self-build mortgages involve staged funding released at key points during the construction process. Lenders assess applications based on factors such as project viability, cost estimates, borrower experience, and contingency planning. Not all lenders offer self-build finance, and criteria can vary significantly across the market.

Examples, scenarios, and market commentary are illustrative only and do not represent any specific lender’s current policy or a guarantee of outcome. Building a property carries financial and project risk, and borrowers should seek appropriate advice before committing to a self-build project.

Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured against it.

Willow Private Finance Ltd is authorised and regulated by the Financial Conduct Authority (FCA No. 588422). Registered in England and Wales.

HSBC's reported pullback from parts of the private credit market highlights why developers, family offices and complex borrowers need specialist funding advice.

Gulf buyers from the UAE, Saudi Arabia and Qatar are returning to London's prime property market. Discover why early finance preparation is becoming increasingly important.

Family offices are increasingly outsourcing specialist expertise as portfolios become more complex. Discover why specialist property finance partners are becoming essential for wealth managers, trustees and private client advisers.

Knight Frank's latest research examines how rental reform and future tax risks are reshaping the prime rental market and why landlords should review their finance strategy.

Discover what the Bank of England's 2026 Financial Stability Report means for high-value borrowers, refinancing, private banking and specialist property finance.

New concerns over mansion tax valuations mean owners of £2m+ homes should review property finance, Lombard lending and wealth planning before the High Value Council Tax Surcharge begins in 2028.

NatWest has completed its £2.7bn acquisition of Evelyn Partners, creating the UK's largest private banking and wealth management business. Discover why specialist property finance partnerships matter more than ever.

Financial Times reports growing use of Lombard lending for property purchases as affluent investors borrow against portfolios instead of selling assets.