Free Consultation. Free Finance Assessment. No Obligation.

At Willow Private Finance, there isno charge to speak to one of our specialist advisorsandno charge for us to assess your requirements and identify suitable finance solutions.

We'll take the time to understand your circumstances, review your objectives and explore the options available to you before you decide whether you want to proceed.

Should you wish to move forward with a recommended solution,any applicable fees will be clearly explained and agreed in advance, ensuring complete transparency from the outset.

Once instructed, we'll manage the process from application through to completion, liaising with lenders, solicitors, valuers and other professionals involved in the transaction to help secure the funding you require.

A lot of high net worth borrowers arrive at the same frustrating point. They have substantial wealth, strong advisers, and a clear property objective, yet a mainstream mortgage application still stalls because the underwriter wants neat PAYE income, simple bonuses, and a standard paper trail.

That problem shows up in different forms. A founder may have most of their wealth in vested shares. A law firm partner may draw income unevenly across the year. A UK national living abroad may earn well in a foreign currency but struggle to satisfy a lender’s verification process. On paper, each is financially strong. In a high street system, each can look awkward.

High net worth mortgages exist for this exact gap. They are not merely “bigger mortgages”. They are a different underwriting discipline, one built around liquidity, asset quality, structure, and the borrower’s wider financial position. The lender is not just asking what landed in your bank account last month. It is asking how your wealth is held, how quickly it can be accessed, how dependable the income sources are, and what the repayment story looks like over time.

That is why two wealthy buyers chasing similar properties can receive completely different outcomes. The difference is rarely just income. It is case presentation, lender fit, and how intelligently the borrowing is structured. This is also why two buyers with the same income can get very different mortgage offers.

Introduction Why Standard Mortgages Fail High Net Worth Borrowers

Standard mortgage systems are designed for volume. They work best when the borrower has salaried income, straightforward outgoings, and a simple UK credit profile.

That is not how many wealthy borrowers operate.

A business owner may keep profits inside the company. An investor may live off drawdowns, dividends, or rental income. A family may hold wealth through trusts, corporate entities, or international structures. These are legitimate, often sensible arrangements. They just do not fit neatly into a retail bank’s checklist.

Where the high street model breaks

The high street tends to reduce affordability to a limited set of inputs. Salary. Bonus history. tax returns. Existing credit commitments. That works for employed borrowers with predictable income. It breaks down when wealth is real but the route to that wealth is less standard.

Typical sticking points include:

Irregular income timing: Quarterly distributions, carried interest, lumpy bonus payments, and retained profits often confuse automated affordability models.

Tax-efficient structuring: Many successful borrowers minimise taxable personal income quite deliberately. Mainstream lenders then understate true borrowing strength.

Asset-heavy balance sheets: Property, portfolios, business interests, and trust assets can be substantial but not always recognised properly by standard underwriting.

Cross-border complexity: Overseas earnings, foreign currency income, and multi-jurisdiction documentation create delays even when the borrower is strong.

A high net worth mortgage case usually fails on presentation before it fails on substance. The wealth may be there. The lender cannot interpret it through a standard process.

Why specialist lending works differently

Private banks and specialist lenders do not start from the same assumptions. They ask better questions. How liquid are the assets? What is the client’s wider banking relationship? Is there a credible exit for an interest-only facility? Can a portfolio support the borrowing without forcing asset sales at the wrong time?

That shift matters. Once the case moves away from a rigid form and into bespoke underwriting, borrowers who looked “difficult” to the high street often become very financeable.

Beyond Income Multiples What Defines a HNW Mortgage?

A high net worth mortgage is defined less by loan size than by underwriting method. The key distinction is that the lender is prepared to assess all aspects of wealth rather than relying only on standard income multiples.

Under UK FCA rules, a borrower can qualify as high net worth by meeting either £300,000 annual income or £3 million in net assets, and lenders may use a debt ratio calculation that derives income by dividing net qualified assets over 84 months.

A core shift is philosophical

A normal residential mortgage is like an MOT. The lender runs through a standard checklist and either the car passes or it does not.

A high net worth mortgage is closer to an engineering review of a specialist vehicle. The lender still checks risk carefully, but it looks at the whole machine. Asset base. Cash reserves. Ownership structures. Liquidity. Repayment strategy. Banking relationship. The answer is not produced by one affordability formula.

First, the lender looks at qualified assets. Not every asset carries the same weight. Cash and marketable investments are easier to use than assets that are hard to value or slow to realise.

Second, the lender tests whether those assets support the requested borrowing and the borrower’s wider obligations. In practical terms, this can mean looking at whether the assets can cover the loan requirement, transaction costs, reserve requirements, and ongoing commitments.

That is where many borrowers get caught out. A large net worth figure on paper is not enough on its own.

Liquidity matters more than headline wealth

Liquidity is often the deciding factor in approval speed and credit appetite.

A listed investment portfolio usually reads well to a lender. A minority stake in a private trading business may not. Overseas holdings inside layered entities can be valuable but cumbersome. A trust can be entirely legitimate yet require detailed legal review before the bank gives it full credit in underwriting.

The strongest HNW mortgage cases are not always the richest. They are the clearest, most liquid, and easiest for the lender to analyse with confidence.

For that reason, borrowers and advisers should stop asking only, “What am I worth?” and start asking, “Which parts of my wealth can this lender rely on?”

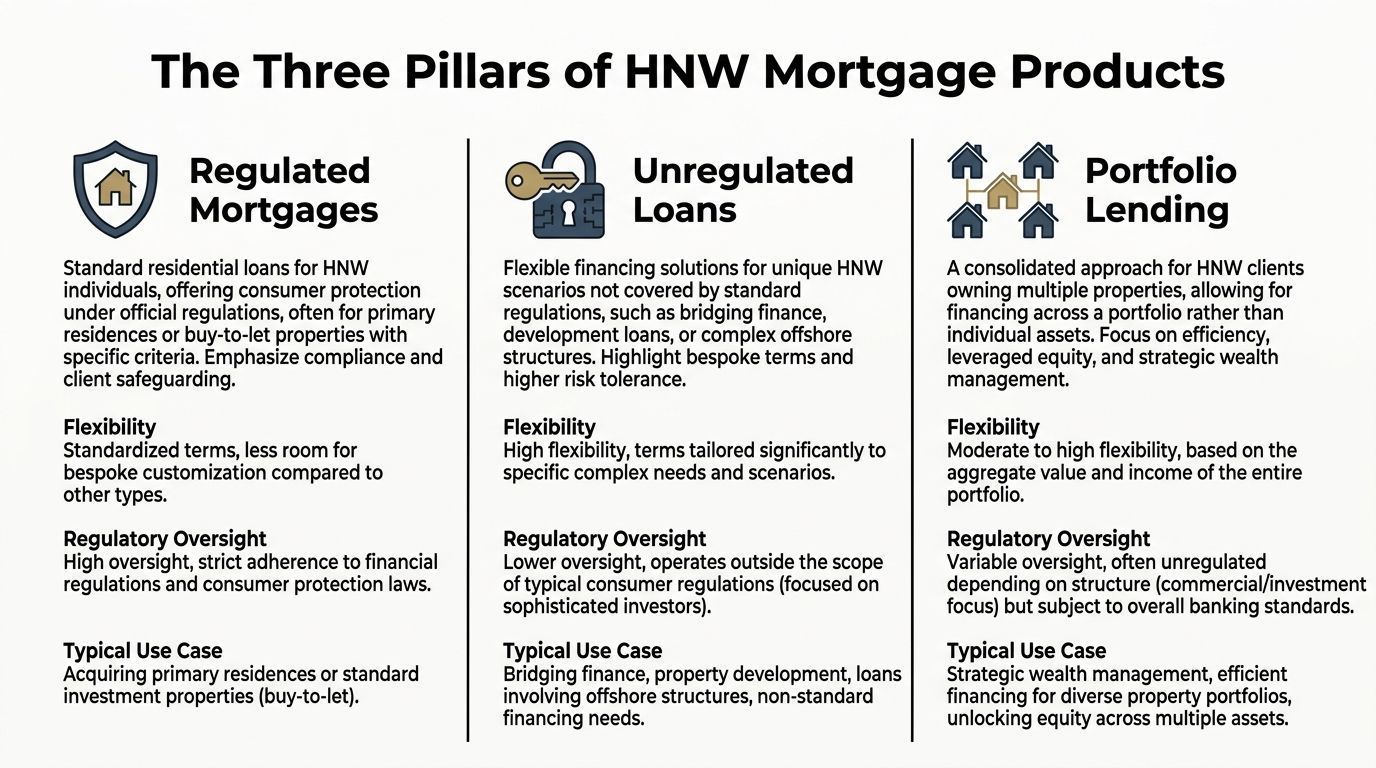

The Three Pillars of HNW Mortgage Products

When people talk about high net worth mortgages, they often lump very different facilities together. In practice, there are three broad routes, and each suits a different type of borrower.

Private bank mortgages

This is the most familiar route for wealthy borrowers buying or refinancing a prime home.

A private bank mortgage is usually relationship-led. The bank wants to understand the client’s wider financial world, not just the property purchase. In return, the borrower may get more flexibility on income interpretation, repayment profile, and overall structuring.

This route tends to work well for:

Senior professionals: Partners, bankers, and executives with variable remuneration.

Business owners: Borrowers with retained profits, dividends, or multiple trading entities.

Clients consolidating relationships: Those willing to place deposits or investments with the bank.

The trade-off is obvious. Private banks can be commercially attractive, but they often prefer clients who bring broader business with them.

Securities-backed lending

This is often the cleanest answer for the asset-rich, income-poor client.

Instead of forcing a sale of investments to raise liquidity, the borrower pledges an investment portfolio and raises finance against that asset base. That can sit alongside a property loan or, in some scenarios, support the property acquisition strategy more directly. The structure is useful when a borrower wants to preserve market exposure, avoid disrupting a portfolio, or move quickly on a purchase.

The right use cases include:

an entrepreneur holding listed shares

a family with a large discretionary portfolio

a client waiting for a liquidity event who does not want to sell early

The risk is also clear. If the underlying portfolio falls sharply, the lender may require action. Securities-backed lending needs active management and proper contingency planning. It is not “cheap money against shares”. It is a specialist structure that can work very well if used properly.

Some clients buy through trusts. Others hold assets through family office structures, offshore companies, or layered ownership vehicles. In these cases, the mortgage is only one part of the problem. The lender must also get comfortable with beneficial ownership, legal capacity, jurisdictional issues, source of wealth, and the path of funds.

This is also where specialist lenders can step in when private banks or high street lenders become too rigid. For asset-rich, income-poor borrowers, specialist lenders can arrange multi-million-pound facilities, including prepaid interest mortgages, particularly for loans in the £2m to £25m range that sit outside mainstream criteria.

Choosing the right pillar

The wrong route usually creates delay, unnecessary scrutiny, or pricing that does not reflect the borrower’s real strength.

A practical way to decide is to ask three questions:

Where is the wealth held? If it sits in managed investments, securities-backed options may be relevant.

How important is flexibility? If the borrower needs customized terms or has unusual ownership, a bespoke structure may be necessary.

Is there a wider banking angle? If the client is open to moving assets or building a relationship, a private bank may sharpen terms.

Product choice should follow wealth structure, not ego. A borrower does not need a private bank mortgage because the property is expensive.

The Art of Private Bank Underwriting

Private bank underwriting is less about boxes and more about judgment. That does not make it loose. In many ways, it is more demanding because the lender wants a full picture, not just a short list of documents.

The borrower’s story matters

A private bank underwriter wants to know how the client made their money, how stable the position is, and what could change.

For a salaried executive, that may be simple. For a founder, it may involve share vesting schedules, business performance, and future liquidity events. For a family office principal, it may involve trust income, investment distributions, and intergenerational planning.

A good case memo does not hide complexity. It explains it.

Asset quality is as important as asset size

Not all assets reassure lenders equally. A substantial listed portfolio is easy to monitor and easier to realise. A prime unencumbered property may support confidence. A minority shareholding in a private company can be valuable but difficult for the bank to rely on in a stress case.

This is why liquidity keeps coming back into the conversation.

Private banks and specialist lenders routinely offer 75% to 85% loan-to-value, and in some circumstances can reach 100% LTV where the borrower has significant liquid assets under the lender’s management. That range is noted in the same earlier reference on HNW underwriting criteria, and it tells you something important. The headline property loan-to-value ratio is often driven by the strength of assets outside the property itself.

Pricing is negotiated, not merely quoted

In the private bank market, pricing can move with the wider relationship. If a client places assets under management with the bank, the credit team may view the case more favourably. That can affect both appetite and terms.

That does not mean every private bank is cheaper. Sometimes a specialist lender wins because it better understands the structure and asks for less relationship commitment. The right answer depends on the client’s priorities.

Why the process feels different

A mainstream lender often gives a yes or no. A private bank often has a conversation first.

That conversation can involve:

Narrative underwriting: How income is generated and why it is sustainable.

Balance sheet analysis: Which assets are liquid, encumbered, pledged, or hard to verify.

Repayment planning: Especially where the facility is interest-only.

Relationship value: Whether the bank sees broader long-term business.

A quick explainer on the mechanics is worth watching before a private bank application starts:

The private bank process works best when the borrower arrives organised, transparent, and realistic about which parts of their wealth the lender will count.

Preparing Your Application A Checklist for Complex Cases

High net worth mortgage applications are won before formal submission. The job is to build a clear credit paper that answers questions before the underwriter asks them.

A significant portion of UK high-net-worth property transactions struggle to complete due to rigid affordability models, often failing because of complex income streams. In practice, many of those failures begin with poor packaging rather than poor credit.

What a lender wants to see

A serious application pack usually includes much more than payslips and bank statements.

Use this as a working checklist:

Personal statement of assets and liabilities: Set out cash, portfolios, property, business interests, loans, guarantees, and contingent liabilities clearly.

Tax documentation: Include relevant personal tax returns and, where needed, supporting documents from more than one jurisdiction.

Income evidence: Show salary, bonus, dividends, partnership drawings, trust income, rental income, or investment distributions in a way the lender can follow.

Business information: If you own companies, provide accounts, management figures where relevant, and an explanation of ownership structure.

Portfolio evidence: For investable assets, provide recent statements and identify what is liquid versus restricted or pledged.

Property schedule: If you already own property, list values, debt, income, and ownership structure.

Repayment strategy: For interest-only borrowing, explain the intended exit clearly and credibly.

Source of deposit and source of wealth: Do not leave this vague. Trace the funds and provide the paper trail.

Common mistakes in complex cases

The weakest submissions usually fail in one of three ways.

First, they overstate net worth but under-explain liquidity. Second, they present documents without interpretation, leaving the underwriter to join the dots. Third, they ignore the legal structure around trusts, overseas entities, or family arrangements until late in the process.

A well-run case includes a short written narrative. It should explain who the borrower is, what the property is for, how the income works, where the wealth sits, and why the requested structure makes sense.

That single step often changes the quality of lender engagement.

Financing UK Property as an Expat or Foreign National

International status does not make a borrower unattractive. It makes the case more technical.

That distinction matters. Many expats and foreign nationals assume they will be declined because they do not fit a normal UK mortgage profile. A key issue is that many lenders are not equipped to assess overseas income, cross-border wealth, and residency complications efficiently.

That figure reflects a familiar pattern. A client may have strong income in dollars, dirhams, or another major currency, but the lender still worries about consistency, convertibility, and documentary reliability.

The four issues lenders focus on

Most cross-border mortgage cases revolve around the same pressure points:

Income verification: Overseas payslips, bonuses, and business accounts often need careful interpretation.

Currency risk: The lender wants comfort that exchange-rate movement will not destabilise affordability.

Residency and jurisdiction: Tax residence, visa status, and country of earnings can all affect lender appetite.

UK footprint: Some lenders want to see an ongoing UK link, whether through citizenship, assets, address history, or banking relationships.

What works in practice

The strongest expat and foreign national cases are usually routed to lenders with dedicated international capability. Those lenders know how to read foreign income documents, how to approach non-UK credit history, and when to lean on a wider asset base rather than narrow salary multiples.

For some clients, debt service from UK rental income can carry more weight than overseas employment income. For others, the answer is a private bank route supported by liquid assets. In more involved cases, specialist brokers such as Willow Private Finance can structure submissions for private banks and niche lenders where foreign currency income, trusts, or multi-jurisdiction wealth would otherwise slow the deal.

Expat borrowing succeeds when the lender is chosen for the jurisdiction as much as for the rate.

HNW Mortgage Case Studies in Action

The theory becomes much clearer when you see how these facilities work in live scenarios. The details below are anonymised and simplified, but they reflect the sort of structuring issues that come up regularly.

The founder with wealth tied up in listed shares

A UK tech entrepreneur wanted to buy a prime London home. On paper, the problem was obvious. Personal taxable income was modest because most value sat in shares and investment accounts. A mainstream lender focused on income multiples would have treated the case as underpowered.

The solution was not to force a sale of shares.

Instead, the case was framed around liquid investments, reserve strength, and the client’s wider financial position. The lender accepted that the borrower was asset-rich, even though ordinary income looked light for the property in question. An interest-only structure made sense because the client wanted to preserve liquidity and avoid disposing of investments at the wrong time.

The lesson was straightforward. Wealth was never the problem. The issue was choosing a lender willing to underwrite the balance sheet properly.

The expat landlord with messy overseas income

Another borrower was a UK national living in the US with several UK rental properties and a plan to refinance and acquire another asset. Their employment income was strong, but documenting and translating that income into a standard UK affordability model was cumbersome.

The better route was to focus the application on the UK property portfolio itself. The lender was more interested in the rental strength, portfolio quality, and borrower track record than in trying to force overseas salary documents into a domestic model.

That removed a lot of friction. Instead of asking the lender to become comfortable with every moving part of a foreign income profile, the case centred on the assets and cash flow that sat within the UK property structure.

The family trust buying a legacy property

A family wanted to acquire a countryside estate through a broader wealth-planning structure. The property decision was tied to trust arrangements, family governance, and the desire to preserve flexibility for future generations.

This was not a case for a standard retail mortgage.

The lender needed to understand the trust deed, the controlling parties, the source of funds, and the rationale for the borrowing itself. Legal review mattered as much as credit appetite. The eventual structure involved a bespoke facility aligned with the family’s ownership and succession planning rather than a generic residential product.

What these examples have in common

These cases look different on the surface, but they share the same core features:

Complexity is normal: Irregular income, layered ownership, and asset concentration are common in HNW borrowing.

The right lender is more important than the broadest brand name: Familiar names do not always mean flexible underwriting.

Case presentation changes outcomes: A clear narrative and properly organised evidence often make the difference.

The mortgage is part of a wider strategy: Borrowing decisions sit alongside tax, liquidity, investment, and estate planning considerations.

High net worth mortgages work best when they solve a broader financial objective, not when they are treated as a standalone commodity purchase.

Conclusion Finding Your Way Forward

High net worth mortgages are not just larger versions of standard home loans. They are specialist solutions for borrowers whose wealth, income, or ownership structures fall outside the high street template.

That is why standard lenders often struggle with successful founders, partners, investors, trustees, expats, and internationally mobile families. The problem is rarely that the borrower lacks substance. The problem is that mainstream systems are built to process simplicity, not sophistication.

The practical route forward is to start with structure, not rate. Work out where the wealth sits. Identify what is liquid. Decide whether the right answer is a private bank, a securities-backed route, a specialist lender, or a bespoke trust or family office structure. Then package the case properly so the lender can understand it quickly.

For borrowers and professional introducers, that is where a specialist broker adds real value. The role is not just sourcing a loan. It is matching the borrower to the correct lending channel, preparing a coherent credit story, managing legal and documentary complexity, and negotiating terms that reflect the true strength of the case.

In this part of the market, poor lender selection wastes time. Poor presentation loses opportunities. Good structuring protects flexibility, preserves liquidity, and can keep a transaction on track when a mainstream route would fail.

If you are considering high net worth mortgages, approach the process as a strategic exercise. The property matters. The loan matters. But the wider balance sheet and long-term plan matter just as much.

📞 Want Help Navigating Today’s Market?

Book a free strategy call with one of our mortgage specialists. We’ll help you find the smartest way forward, whatever rates do next.

Tailored advice for individuals, businesses and professional advisers seeking sophisticated financial solutions.

At Willow Private Finance, we understand that every client has different ambitions, financial circumstances and long-term objectives. Whether you are purchasing property, refinancing existing borrowing, protecting your family or business, or looking to unlock wealth through specialist lending, we build solutions around your individual needs rather than forcing you into standard products.

As an independent, whole-of-market brokerage, we provide access to residential mortgages, buy-to-let finance, bridging loans, development finance, commercial lending, private banking and Lombard lending facilities, alongside a comprehensive range of personal and business protection solutions. Our expertise extends to UK and international clients, high-net-worth individuals, company directors, investors, expatriates and borrowers with complex financial structures.

By combining deep technical expertise with relationships across mainstream lenders, specialist lenders and private banks, we help clients secure funding, structure borrowing efficiently and protect the assets, income and people that matter most. Whatever stage of your financial journey you are at, our team is here to provide clear, strategic advice that delivers confidence and long-term value.

From mortgages and private banking to Lombard lending, business finance and protection planning, Willow Private Finance delivers bespoke solutions for even the most complex financial requirements.

Wesley Ranger is a senior finance professional with over 20 years’ experience in the UK mortgage and specialist lending markets. As a director at Willow Private Finance, he has extensive experience advising high-net-worth individuals on complex and large-scale property finance.

His expertise includes structuring mortgages for clients with multiple income streams, international assets, trust structures, and non-standard financial profiles. Wesley has worked with private banks, specialist lenders, and international funding sources to secure finance for high-value residential and investment properties.

He has a detailed understanding of how lenders assess high-net-worth clients, including asset-backed lending, bespoke underwriting, and risk analysis beyond standard affordability models. His experience spans both UK and cross-border transactions, providing a comprehensive, whole-of-market perspective.

Wesley regularly advises on structuring lending solutions that align with broader wealth planning strategies, ensuring that financing decisions support long-term financial objectives.

Important Notice

This article is for general information purposes only and does not constitute personal financial advice, tax advice, or legal advice. Mortgage availability, criteria, and rates depend on individual circumstances and may change at any time.

High net worth mortgages often involve bespoke underwriting, including detailed assessment of income, assets, liabilities, and overall financial position. Lenders may apply flexible or non-standard criteria, but not all borrowers will be eligible for specialist lending solutions.

Examples, scenarios, and market commentary are illustrative only and do not represent any specific lender’s current policy or a guarantee of outcome. Borrowers should seek appropriate advice when arranging large or complex borrowing, particularly where financial structures involve international elements or non-standard income.

Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured against it.

Willow Private Finance Ltd is authorised and regulated by the Financial Conduct Authority (FCA No. 588422). Registered in England and Wales.

Julius Baer's Global Wealth and Lifestyle Report 2026 highlights why currency, international mobility and cross-border wealth are reshaping property finance for expats, foreign nationals and HNW borrowers.

The Bank of England's latest Financial Stability Report explains why collateral, leverage and liquidity matter for Lombard lending, securities-backed finance and high-net-worth borrowers.

HSBC's reported pullback from parts of the private credit market highlights why developers, family offices and complex borrowers need specialist funding advice.

Gulf buyers from the UAE, Saudi Arabia and Qatar are returning to London's prime property market. Discover why early finance preparation is becoming increasingly important.

Family offices are increasingly outsourcing specialist expertise as portfolios become more complex. Discover why specialist property finance partners are becoming essential for wealth managers, trustees and private client advisers.

Knight Frank's latest research examines how rental reform and future tax risks are reshaping the prime rental market and why landlords should review their finance strategy.

Discover what the Bank of England's 2026 Financial Stability Report means for high-value borrowers, refinancing, private banking and specialist property finance.