Free Consultation. Free Finance Assessment. No Obligation.

At Willow Private Finance, there isno charge to speak to one of our specialist advisorsandno charge for us to assess your requirements and identify suitable finance solutions.

We'll take the time to understand your circumstances, review your objectives and explore the options available to you before you decide whether you want to proceed.

Should you wish to move forward with a recommended solution,any applicable fees will be clearly explained and agreed in advance, ensuring complete transparency from the outset.

Once instructed, we'll manage the process from application through to completion, liaising with lenders, solicitors, valuers and other professionals involved in the transaction to help secure the funding you require.

Master Your Buy To Let Interest Only Mortgages Calculator

A familiar scene plays out every week. A landlord finds a property that looks right on paper, opens a buy to let interest only mortgages calculator, plugs in the loan amount and rate, and gets a neat monthly payment figure that seems manageable.

That number is useful. It is also incomplete.

For an experienced investor, the key question is not whether the monthly interest looks affordable in isolation. The more important question is whether the deal survives lender stress testing, leaves enough cash flow after real-world costs, and works when rates move, rents soften, or the lender reviews the wider portfolio. That is where many online calculators stop being decision tools and become false reassurance.

Beyond the Basics Why a Standard Calculator Is Not Enough

A landlord agrees a purchase at a yield that looks fine on a simple calculator, then finds the case trims down once the lender applies its own rate, rent test, and portfolio view. That gap between a neat payment result and an underwriter’s conclusion is where good deals get reshaped and weak ones fall away.

Interest-only borrowing remains popular in buy to let for a practical reason. It keeps monthly payments lower and preserves cash flow that can be used for voids, works, tax, or the next acquisition. But a calculator that only shows the monthly interest cost does not tell you how a lender will read the case.

Professional investors use the calculation differently. They do not ask only, "What is the payment?" They ask whether the loan still fits if the lender stresses the rate above the product pay rate, whether rental coverage still clears the required margin, and whether the property sits cleanly within the lender’s appetite for single lets, HMOs, limited companies, or larger portfolios.

That matters because lender logic is not uniform. A high street buy to let case and a specialist funding route can produce different borrowing outcomes from the same property, rent, and deposit. One lender may focus narrowly on the subject property. Another may examine the wider portfolio, existing debt exposure, background income, liquidity, and the borrower’s exit options.

A standard calculator gives you a starting figure. An investor-grade assessment shows pressure points.

Used properly, a calculator becomes an underwriting rehearsal. It helps test whether the structure is likely to hold before you spend money on valuation fees, legal work, and arrangement costs. It also helps you spot where a small change in loan size, ownership structure, or rent assumption could move the case from marginal to workable.

If you are reviewing options in the buy-to-let mortgage market, use the calculator to screen for resilience, not just affordability. That approach is especially useful for portfolio landlords and higher-net-worth investors, where the opportunity often sits in the gaps a basic calculator fails to measure.

A calculator earns its keep when it filters out a weak structure early and highlights where better terms, lower gearing, or a different lender strategy can improve the deal.

BTL Stress Test Calculator

LTV: 75%

Actual rate you will pay monthly

Rate used for underwriting (e.g. 5.5% or Pay Rate + 2%)

Monthly Payment (Interest Only):£0.00

Actual Net Cash Flow (Est):£0.00

Calculated ICR:0%

Checking...

Mastering the Inputs for an Accurate Financial Picture

A landlord spots a flat that looks attractive on paper. The asking rent appears strong, the interest-only payment looks manageable, and the headline loan size seems to fit. Then the valuation comes in lower than expected, the lender applies a stressed rate rather than the pay rate, and the case no longer works at the original debt-to-value ratio.

That gap comes from the inputs, not the calculator.

Start with the value a lender is likely to recognise

Property value is rarely just a box to fill in.

For a purchase, the lender may base the case on the lower of the agreed price and the surveyor’s valuation. For a remortgage, current market value drives the gearing calculation. If your numbers only work at an optimistic figure, the structure is weak before underwriting even starts.

I test the deal against the lower value first. That gives a cleaner view of whether the borrowing plan survives a cautious assessment.

Deposit size changes more than the loan amount

Many investors begin with a target LTV and work backwards. That is a reasonable starting point, but it is not a strategy on its own.

A higher deposit does three jobs at once. It reduces borrowing exposure. It improves the stressed interest calculation. It leaves more room if the lender values conservatively or if rents are assessed with less generosity than expected. For portfolio landlords, that extra margin can matter more than squeezing out the last tranche of borrowing on one purchase.

Three deposit questions help sharpen the analysis:

What is the minimum needed to meet the lender's LTV cap?

What level gives the rent enough headroom under stress testing?

What level still leaves liquidity for refurbishments, tax, voids, and the next acquisition?

That third point is often missed. An investor can overfund a deposit and weaken the wider portfolio.

Enter the rate used for underwriting, not just the rate on the illustration

A basic calculator often encourages the wrong habit. It invites the user to enter the product rate and stop there.

That is only part of the picture. Lenders assess buy-to-let cases using a stressed or notional rate, and that can be higher than the initial deal rate. The result is straightforward. A case that looks comfortable on monthly interest can still fail the lender's rental test.

Use two separate rate assumptions every time:

The pay rate, to estimate the actual monthly cost during the initial term

The stress rate, to judge whether the case is likely to pass underwriting

For interest-only payment modelling, the underlying maths is simple. Annual interest is the loan multiplied by the rate. Divide that figure by 12 for the monthly cost. Useful, but incomplete. Professional use of a calculator means checking both cash cost and lender stress cost side by side.

On interest only, the balance remains outstanding throughout the term. The loan does not solve itself.

So the term has to match the investment plan. If the likely exit is sale after refurbishment and stabilisation, that points to one structure. If the intention is long-term hold and refinance, that points to another. Older borrowers, limited company applicants, and higher-value cases can all face lender-specific rules on maximum age, term length, and repayment strategy.

A longer term can improve flexibility. It can also postpone a problem rather than solve it. The right setting depends on how the debt will be cleared or replaced later.

Rent should be input with discipline, not optimism

Typing in the advertised rent is lazy analysis.

Use the rent the property can realistically achieve in its present condition, supported by local evidence if possible. Then pressure-test it. What happens if the valuer takes a slightly lower view. What happens if the first tenancy starts later than planned. What happens if incentives or refurbishment mean full rent is not available from day one.

Lenders focus on whether rent covers stressed mortgage interest. Investors need a second lens. They need to know whether the rent still leaves enough surplus after the actual friction in the asset.

Costs belong in the model from day one

A deal is not profitable because the mortgage payment looks low.

Public calculators often miss the actual operating drag that determines whether a property performs well in practice. Add those costs yourself, even if the tool does not ask for them:

Letting or management fees

Service charge and ground rent

Buildings insurance

Maintenance and compliance costs

Voids and arrears allowance

Refurbishment period with delayed rent

Accountancy and company administration costs where relevant

Experienced investors separate an acceptable acquisition from a funding trap. A property can pass a simple mortgage test and still be poor business once all cash demands are counted.

Accurate inputs produce a decision-quality result. Optimistic rent, light costs, and the wrong interest rate produce a false green light.

Related Guide

Buy-to-Let Finance Depends On More Than The Monthly Mortgage Payment

As this article explains, a buy-to-let investment can look attractive on basic figures but fail once lender stress rates, valuation assumptions, rental coverage and real operating costs are properly assessed. The difference between a strong investment and a funding problem often comes down to using realistic inputs before committing to the purchase.

Our Buy-to-Let Mortgage Guide explains how lenders assess rental income, interest coverage ratios, loan-to-value, limited company borrowing, portfolio landlords and refinancing strategies, helping investors structure finance around sustainable cash flow rather than optimistic headline numbers.

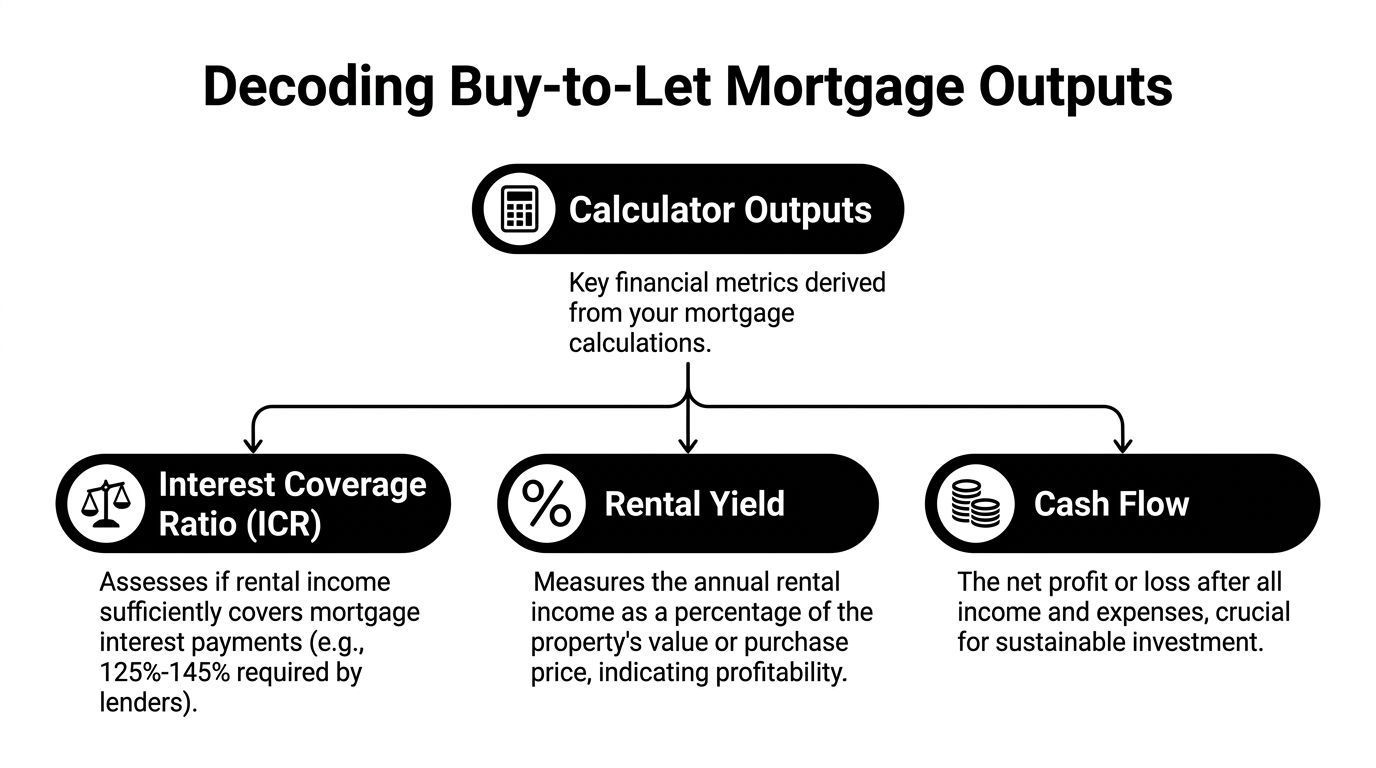

Decoding the Outputs Interest Coverage Ratio Yield and Cash Flow

A landlord agrees a purchase at a price that looks sensible, the rent seems strong, and the interest-only payment appears comfortable.

Then the lender sizes the case off stressed interest rather than the pay rate, trims the usable rent, and the expected loan falls short. That is why the outputs matter more than the headline payment.

Interest Cover Ratio decides whether the case works

Interest Cover Ratio, or ICR, is the first output to read because it determines whether the lender will support the loan at the amount you want.

ICR measures annual rent against annual stressed mortgage interest, not necessarily the initial product payment. That distinction catches investors out. A deal can look comfortable on day-one cash flow and still fail the lender's rental test because the underwriting rate and minimum coverage requirement are less forgiving than the actual pay rate.

The logic is simple:

Annual rent

divided by

annual stressed interest

The result must clear the lender's minimum threshold for that borrower profile, ownership structure, and property type.

A straightforward example shows why this matters. If a property produces £18,000 a year in rent and the lender calculates stressed annual interest at £12,000, the ICR is 150%. Whether that passes depends on the lender's policy. For one lender it may be acceptable. For another, especially with higher-rate taxpayer assumptions or a weaker property type, it may still be tight.

Professional investors read ICR as more than a pass or fail number. It also signals borrowing efficiency. A high ICR can mean room to raise the loan, improve terms, or place the case with a wider set of lenders. A thin ICR limits options and weakens your refinance position later.

Yield answers a different question

Yield does not tell you whether the lender will lend. It tells you whether the asset earns enough to justify the capital tied up in it.

Gross yield is a quick screening tool. It compares annual rent to purchase price or current value and helps rank opportunities across a pipeline. That is useful, but it is still only a surface measure.

Net yield carries more weight because it reflects the costs the property drags behind it. A flat with a respectable gross yield can become mediocre once service charge, management, insurance, licensing, and routine maintenance are included. A house with a lower headline yield can outperform if the cost base is cleaner and the rent is more stable.

Use yield to compare assets. Use ICR to judge financeability. Use both before deciding how much equity the deal deserves.

Cash flow shows whether the deal serves your strategy

Cash flow is where lender logic and investor logic part company.

A property can pass ICR comfortably and still be a poor hold if the actual monthly surplus is too narrow to cover repairs, voids, tax friction, and future refinancing costs. I see this regularly with deals that were bought for maximum debt financing rather than durable income.

Read cash flow through three filters:

Funding filter. Does the property support the loan size you need?

Operating filter. Does the monthly surplus remain worthwhile after all known costs?

Portfolio filter. Does that surplus strengthen liquidity across the wider portfolio, or does it trap cash in a marginal asset?

That third question matters more for portfolio landlords and HNW investors than many calculators acknowledge. A single unit with modest surplus may be acceptable in isolation. Inside a larger portfolio, it can still be inefficient if it consumes management time, weakens average ICR, or limits future borrowing capacity.

Read the outputs in a broker's order

The sequence matters because each output answers a different commercial question.

Start with maximum loan available, because that tells you whether the deal can be structured at the debt financing level you want. Then check ICR, because a workable loan size still needs to clear the lender's rental stress. After that, look at the monthly interest payment at the likely product rate, then your net monthly cash flow, then yield as the final quality check against your return target.

That order reflects how a broker assesses a case for placement and how a disciplined investor assesses it for retention.

If the rental stress does not work, the case needs a different structure, more equity, or a different lender. If the rental stress works but surplus cash is thin, the property may still fail your investment brief.

Public tools often stop at a basic payment and a simple rental ratio. Better analysis asks what those outputs mean across lender choice, refinance risk, and portfolio resilience. For a closer look at that underwriting logic, see this guide to buy to let debt service cover and ICR stress testing.

How to Stress Test Your Investment Like a Professional

A single calculator result is a snapshot. An investor needs a moving picture.

The most useful way to work with a buy to let interest only mortgages calculator is to run several versions of the same deal. Not because you expect every downside to occur at once, but because weak structures reveal themselves when assumptions are tightened.

Run a rate-rise scenario

Start with the base case. Enter the intended loan, likely rent, and actual product rate to understand near-term monthly cost.

Then increase the interest rate to reflect a future market rise and recalculate. The purpose is to know what happens when the fixed rate ends and the refinance market is less forgiving.

The questions to ask are practical:

Does the monthly interest remain comfortably covered by rent?

Does the deal leave a usable monthly surplus after costs?

If you were refinancing at that higher rate, would the likely ICR look workable?

This is not academic stress testing. It tells you whether the current deal relies on the market staying benign.

Cut the rent and watch what breaks

Reduce the rent by a notable percentage.

That tests a softer market, a lower achieved rent after tenant turnover, or a period where the property cannot command the original headline figure. It also acts as a rough proxy for voids and friction where a calculator does not allow separate entries.

A resilient deal should look coherent under this scenario. The answer does not need to be perfect. It needs to be manageable.

Stress testing is less about predicting the future and more about identifying the assumptions your deal cannot survive.

The single-property calculator starts to break down once you own several properties.

Standard calculators often miss the portfolio-wide stress testing used by lenders, including lender-specific rules such as Aldermore’s 160% ICR for HMOs and Barclays’ integrated affordability assessment across all mortgages. The same source states that 68% of landlords with 5+ properties report inaccurate calculator estimates leading to borrowing projection issues and application rejections.

That is why experienced investors should not model each property in isolation.

Portfolio underwriting can look at:

The strength or weakness of the wider rental book.

Concentration risk by property type.

Overall debt across the portfolio.

Whether one marginal asset is being subsidised by stronger properties or external income.

If one property has a weaker ICR but the wider case is strong, some lenders may still engage. Others will not. A public calculator cannot tell you which camp your chosen lender falls into.

This video gives a practical backdrop to the way interest-only borrowing needs to be considered in the round, rather than as a single monthly number.

A simple professional routine

When assessing any deal, run at least four versions:

Base case using your likely product rate and realistic rent.

Refinance case with the rate moved higher.

Soft-rent case with rent reduced.

Combined pressure case with both changes applied together.

A deal that works only in version one is fragile. A deal that behaves sensibly across all four has financing resilience.

Connecting the Calculator to Real-World Lender Criteria

Even an accurate calculator does not issue mortgage offers. Lenders do. Their criteria do not always sit neatly inside public tools.

A calculator pass is not a lender pass

A public tool can estimate whether rent covers stressed interest. It cannot always tell you whether the lender likes the property, borrower profile, ownership structure, or wider exposure.

That gap matters most in cases involving:

Portfolio landlords, where lenders may assess the whole book.

Expats and international borrowers, where income sourcing and documentation can be more complex.

High-value cases, where underwriting may become more bespoke.

HMOs and multi-unit property, where lender policy diverges sharply.

A landlord may appear to pass on a standard calculator and find the lender trims the loan because the case falls into a stricter internal category.

Specialist lenders and private banks play by different rules

Here, market knowledge starts to matter more than calculator literacy.

For complex or high-value cases, private banks may apply lower ICRs of 100% to 115% by using top-slicing from other income sources or securities-backed lending, and that this bespoke structuring can increase approval rates by up to 30% compared with high street lenders using rigid calculator metrics.

That does not mean every investor should chase a private bank solution. It means the visible high street answer is not always the actual market answer.

Top-slicing can be relevant where the property is strong but the rent alone does not fully satisfy a mainstream stress test. A borrower with earned income, investment income, or wider assets may have options that a retail calculator cannot surface.

Expat and HNW borrowing need context, not just numbers

For expats, the issue is less about the property and more about the way income is verified, translated, and accepted. A calculator cannot assess jurisdictional complexity, foreign currency exposure, or how individual lenders treat overseas earnings.

For high-net-worth clients, the limitation is different. Wealth can improve the credit story, but only if the lender knows how to underwrite it. Public calculators ignore liquid assets, securities portfolios, trust structures, and family-office backed arrangements.

That is why a buy to let interest only mortgages calculator should be viewed as one layer in a broader decision process.

Good structuring often means selecting the right underwriting philosophy, not just the cheapest headline rate.

A landlord buys on interest-only because the monthly payment works. Five, ten, or fifteen years later, the ultimate test is whether the structure still works after tax and whether the exit is still credible.

That is the part basic calculators handle poorly.

They are good at showing a monthly interest cost. They are weaker on the questions that decide long-term success. How much net income remains after tax. Whether profits are being retained or drawn. Whether the property will still refinance cleanly if rates stay higher for longer. Whether the repayment plan would stand up to lender scrutiny rather than just sounding plausible on paper.

Tax can turn a pass into a weak hold

Section 24 changed the economics for landlords holding property personally. Mortgage interest relief is no longer given in the old way, so a deal that looks acceptable on a pre-tax calculator can produce less disposable profit than expected.

The change has pushed an estimated 42% of BTL investors into higher tax brackets. That matters because many landlords still test deals on rental surplus before tax, then wonder why retained cash never builds as planned.

Professional investors separate the analysis properly:

Does the rent support the debt?

What is the post-tax cash position?

Are profits being kept inside the structure or taken out?

Does the ownership structure still make sense for the next refinance, not just this purchase?

That is why I do not treat an interest-only calculator as a simple affordability tool. I use it as the first screen, then pressure-test the tax drag and the repayment route behind it.

Repayment plans need evidence, not good intentions

With interest-only borrowing, the capital balance is still there at the end of the term. Lenders know this. Larger loan sizes make the point sharper, not softer.

A vague answer such as "I will probably sell" or "I can always refinance" is weak because both routes depend on future conditions you do not control. Sale depends on market timing, tax exposure, and equity. Refinance depends on age, rates, rental coverage, property type, and lender appetite at that point.

Stronger repayment strategies are specific and evidenced:

Sale of the property: works best where the property is clearly an investment asset, the equity buffer is healthy, and the disposal timing fits the wider portfolio plan.

Refinance at term end: works where borrowing levels have been kept sensible and the property is likely to remain financeable under future stress tests.

Repayment from other assets: works where liquid investments, business proceeds, or other realisable assets can be demonstrated and are not already committed elsewhere.

The trade-off is straightforward. Interest-only improves short-term cash flow and can increase portfolio flexibility. It also leaves you carrying refinancing risk, valuation risk, and end-of-term execution risk for much longer.

For personally held property, tax friction can restrict how much cash you retain over time, which weakens both resilience and repayment options. For limited company investors, interest deductibility is more favourable, but the structure still needs a clear exit plan, realistic cash retention, and a repayment method a lender would accept if asked to review it today.

Your Next Move From Calculation to Consultation

Used well, a buy to let interest only mortgages calculator is one of the most useful tools in a landlord’s toolkit. It can show whether rent covers debt, whether the loan amount is sensible, and whether a deal deserves further work.

Used casually, it can do the opposite. It can make a thin deal look acceptable because the assumptions were generous or the lender logic was shallow.

The professional approach is straightforward. Enter realistic values. Model lender stress, not just product pricing. Test the downside. Read ICR before monthly payment. Then compare the result against actual lender criteria, ownership structure, tax reality, and your repayment plan.

The best borrowing outcomes come from good preparation rather than last-minute problem solving. When the numbers are disciplined before the application starts, the lender conversation is cleaner and the strategy is stronger.

📞 Want Help Navigating Today’s Market?

Book a free strategy call with one of our mortgage specialists. We’ll help you find the smartest way forward, whatever rates do next

Tailored advice for individuals, businesses and professional advisers seeking sophisticated financial solutions.

At Willow Private Finance, we understand that every client has different ambitions, financial circumstances and long-term objectives. Whether you are purchasing property, refinancing existing borrowing, protecting your family or business, or looking to unlock wealth through specialist lending, we build solutions around your individual needs rather than forcing you into standard products.

As an independent, whole-of-market brokerage, we provide access to residential mortgages, buy-to-let finance, bridging loans, development finance, commercial lending, private banking and Lombard lending facilities, alongside a comprehensive range of personal and business protection solutions. Our expertise extends to UK and international clients, high-net-worth individuals, company directors, investors, expatriates and borrowers with complex financial structures.

By combining deep technical expertise with relationships across mainstream lenders, specialist lenders and private banks, we help clients secure funding, structure borrowing efficiently and protect the assets, income and people that matter most. Whatever stage of your financial journey you are at, our team is here to provide clear, strategic advice that delivers confidence and long-term value.

From mortgages and private banking to Lombard lending, business finance and protection planning, Willow Private Finance delivers bespoke solutions for even the most complex financial requirements.

Wesley Ranger is a senior finance professional with over 20 years’ experience in the UK mortgage and specialist lending markets. As a director at Willow Private Finance, he has extensive experience advising property investors on buy-to-let finance, including interest-only mortgage structures.

His expertise includes structuring landlord borrowing to optimise cash flow, assessing lender stress testing models, and aligning mortgage terms with investment strategy. Wesley has worked with both new and experienced landlords, from single-property investors through to those managing large portfolios.

He has a detailed understanding of how lenders assess interest-only buy-to-let applications, including rental coverage ratios, stress rates, and portfolio exposure. His experience spans high street lenders, specialist providers, and private funding sources, providing a comprehensive, whole-of-market perspective.

Wesley regularly advises on structuring investment finance to balance yield, risk, and long-term portfolio growth.

Important Notice

This article is for general information purposes only and does not constitute personal financial advice, tax advice, or legal advice. Mortgage availability, criteria, and rates depend on individual circumstances and may change at any time.

Interest-only buy-to-let mortgages involve paying only the interest on the loan during the term, with the capital repaid at the end. Lenders assess affordability based on rental income, stress testing, and borrower profile. Not all borrowers will meet these criteria, and lending terms may vary significantly between providers.

Any calculator outputs or examples are illustrative only and do not reflect actual lender offers or guarantees. Investors should carefully consider the risks associated with interest-only borrowing, particularly where repayment depends on future property sale or refinancing.

Julius Baer's Global Wealth and Lifestyle Report 2026 highlights why currency, international mobility and cross-border wealth are reshaping property finance for expats, foreign nationals and HNW borrowers.

The Bank of England's latest Financial Stability Report explains why collateral, leverage and liquidity matter for Lombard lending, securities-backed finance and high-net-worth borrowers.

HSBC's reported pullback from parts of the private credit market highlights why developers, family offices and complex borrowers need specialist funding advice.

Gulf buyers from the UAE, Saudi Arabia and Qatar are returning to London's prime property market. Discover why early finance preparation is becoming increasingly important.

Family offices are increasingly outsourcing specialist expertise as portfolios become more complex. Discover why specialist property finance partners are becoming essential for wealth managers, trustees and private client advisers.

Knight Frank's latest research examines how rental reform and future tax risks are reshaping the prime rental market and why landlords should review their finance strategy.

Discover what the Bank of England's 2026 Financial Stability Report means for high-value borrowers, refinancing, private banking and specialist property finance.