Free Consultation. Free Finance Assessment. No Obligation.

At Willow Private Finance, there isno charge to speak to one of our specialist advisorsandno charge for us to assess your requirements and identify suitable finance solutions.

We'll take the time to understand your circumstances, review your objectives and explore the options available to you before you decide whether you want to proceed.

Should you wish to move forward with a recommended solution,any applicable fees will be clearly explained and agreed in advance, ensuring complete transparency from the outset.

Once instructed, we'll manage the process from application through to completion, liaising with lenders, solicitors, valuers and other professionals involved in the transaction to help secure the funding you require.

You are looking at the same problem many buyers are facing in 2026. The property you want is not wildly out of reach in headline terms, but the full deposit, the lender’s affordability model, and the monthly payment all pull in the wrong direction at once.

That is where shared ownership becomes more interesting than many people assume. It is often described as a fallback for buyers who cannot purchase outright. In practice, the better way to view it is as a financing structure. If used properly, it can reduce the upfront cash requirement, contain the mortgage balance, and create a path to fuller ownership later.

The difficulty is not understanding the broad idea. Many grasp the part-buy, part-rent concept quickly. The challenge involves understanding shared ownership mortgage rates, why they can differ from standard residential pricing, and how lenders assess the risk.

That is where deals are won or lost. A borrower who understands the lender’s view of lease terms, affordability, income quality, and future staircasing options will usually make better decisions than someone who focuses only on the initial monthly figure.

Is Shared Ownership the Smartest Way onto the Property Ladder

A common scenario looks like this. A buyer has solid income, sensible spending habits, and a deposit that would normally be respectable. Then they apply that deposit to a full market purchase and realise the numbers no longer work cleanly. The loan is too large, the stress test is too tight, or the property type creates extra caution from the lender.

In those cases, shared ownership can be the smarter structure rather than a reluctant compromise.

The reason is straightforward. You are not trying to force a full-ownership mortgage onto a balance sheet that does not comfortably support it. You are buying a defined share and financing only that share. That changes the shape of the case from day one.

For many buyers, the decision is not “buy or keep renting”. It is closer to this:

Use all available capital now on a full purchase and accept a tighter affordability position.

Use less capital upfront on a shared ownership purchase and keep more liquidity.

Enter the market in stages rather than waiting for the perfect full-ownership scenario.

That third route often gets dismissed too quickly.

A good shared ownership case works best when the buyer treats the first purchase as the opening move, not the final destination. If the lease terms are sensible, the rent review mechanism is understood, and the mortgage product is chosen with future remortgaging in mind, the structure can be efficient.

There are also situations where it is not the right answer. If the lease is restrictive, service charges are heavy, or the borrower expects to move again quickly, the apparent affordability can be less attractive in practice. The structure only works when the legal and lending details support it.

Practical takeaway: Shared ownership makes the most sense when it improves affordability without trapping you in a poor lease or an inflexible mortgage.

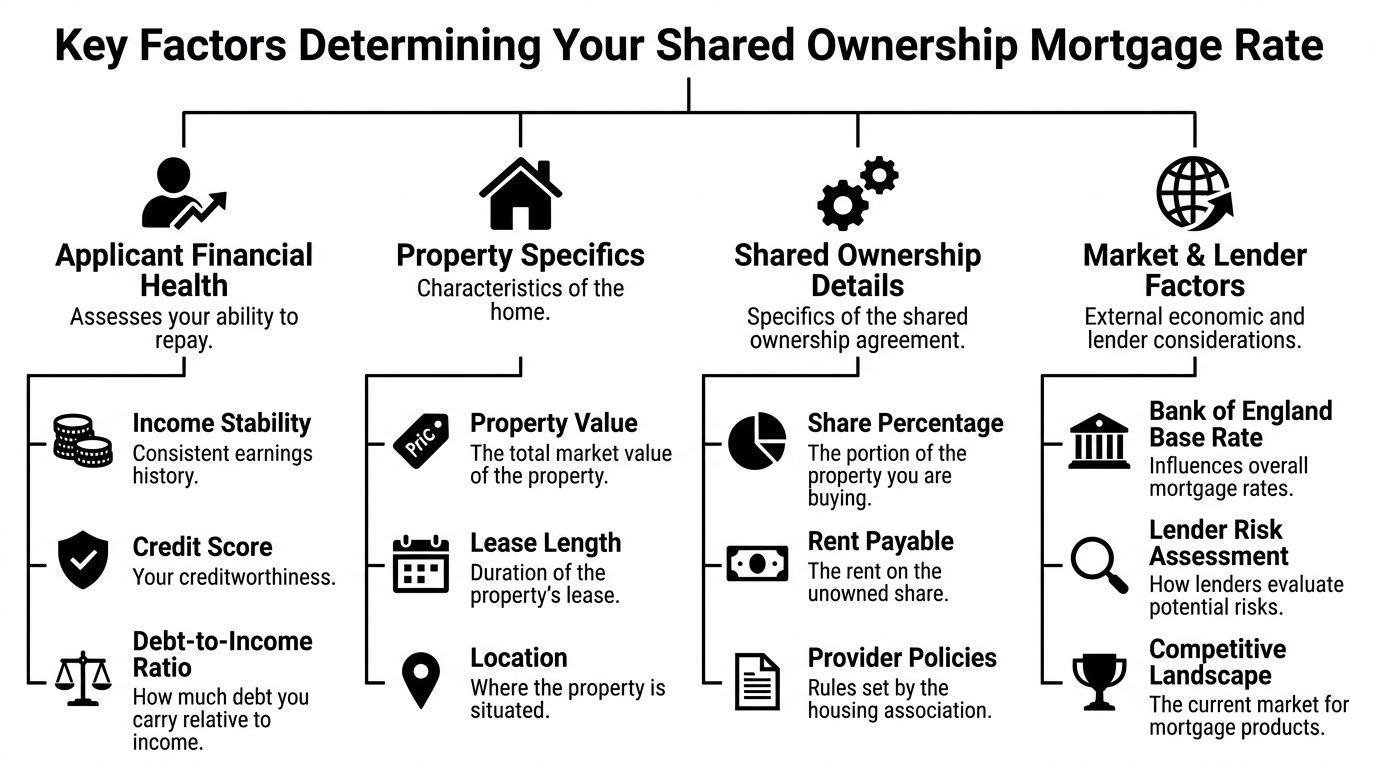

How Shared Ownership Mortgage Rates Are Calculated

A lender can price two shared ownership cases on the same development quite differently, even if the buyers are purchasing the same initial share. The rate is not built from the property price alone. It comes from how the lender assesses the risk of that specific share, lease, housing association, and borrower profile.

The starting point is simple. Interest is charged only on the share you are buying, not on the full market value of the property.

The mortgage is secured against your share

If you buy a 40% share, the mortgage is secured against that 40% purchase. You then pay rent on the remaining share, usually to the housing association, plus any service charge and other property costs.

That means the lender is looking at a split housing commitment, not a standard owner-occupier structure.

Mortgage payment on the share you own

Rent payment on the unsold share

Service charges and other fixed property costs

This lower starting loan amount is why shared ownership can improve entry affordability. It does not automatically mean the rate will match the cheapest mainstream residential pricing.

Why the pricing often sits above standard residential rates

From the lender’s side, shared ownership carries extra layers of risk.

The property is held under a lease that has to meet the lender’s criteria. The lender also has to be comfortable with the housing association, the nomination period, any restrictions on resale, and the practical route to possession and sale if the loan ever defaults. A clean, familiar lease on a scheme the lender already knows is easier to price sharply than a case that needs legal sign-off and manual underwriting.

That is the part many mainstream articles miss. The loan may be smaller, but the security is more specialised.

Rates are also affected by the wider mortgage market. Fixed rates rise and fall with funding costs and swap pricing, not just with your personal profile. For context on that wider mechanism, this guide on how global bond markets move UK mortgage pricing explains why lender pricing can change even when the property and borrower do not.

What lenders price

In practice, lenders are testing four things at once.

Security quality They want a lease and property they can lend on without unusual legal risk.

Affordability across the full structure They assess the mortgage, rent, service charge, credit commitments, and living costs together.

Operational simplicity Cases that fit a lender’s standard shared ownership policy usually price better than those requiring exceptions.

Exit risk If the lender ever had to recover the debt, they need confidence the property could be sold within the lease framework.

This matters even more for complex borrowers. Expats, foreign currency earners, self-employed applicants with layered income, and high net worth clients using trust or bonus-led income often assume a stronger profile guarantees a better rate. Sometimes it does. Sometimes the opposite happens. A lender may like the net worth but still price cautiously if the income is hard to verify in UK-format terms or if the case sits outside its automated policy.

The practical strategy is to shape the case around lender appetite, not just headline affordability. That can mean choosing a larger initial share to improve the risk profile, reducing unsecured commitments before application, presenting foreign income in a format underwriting teams can follow quickly, or selecting a lender with a proven track record on higher-value or internationally sourced income. In shared ownership, the cheapest rate usually goes to the case that looks easiest to underwrite and easiest to exit, not just to the borrower with the highest income.

Related Guide

Shared Ownership Is Just One Route Into Home Ownership

As this guide explains, shared ownership is far more than a way of reducing your deposit. Mortgage rates, lender affordability assessments, lease terms, service charges and future staircasing opportunities all influence whether the structure genuinely supports your long-term plans. Choosing the right lender can often make as much difference as choosing the right property.

Our Residential Mortgages Guide explores how lenders assess affordability, complex income, deposits and borrowing structures, helping first-time buyers and home movers understand the full range of mortgage options available before committing to a shared ownership purchase.

A quoted rate is rarely just about whether you are buying a shared ownership home. It is about how cleanly your case fits the lender’s appetite.

Two buyers can apply for a similar property and receive materially different options because the lender is pricing several layers of risk at once.

Loan to value on the share

This is one of the first filters.

In shared ownership, lenders focus on the loan-to-value against the share being purchased, not just the full property value. A stronger deposit on the purchased share usually helps because the lender has more equity cushion against that loan.

That does not automatically produce the cheapest deal. It does, however, improve the shape of the risk.

The share size itself

The size of the initial share changes more than the maths. It changes lender perception.

A smaller share may lower the mortgage balance, but it also leaves a larger rent element. Some lenders are comfortable with that. Others become more conservative once rent and service charges consume too much of the affordability calculation.

Larger shares can appeal more to certain lenders, especially where the borrower has stronger income and wants a cleaner route toward future remortgaging or staircasing.

Credit profile and income quality

Shared ownership underwriting is not only about whether you pass credit score thresholds. Lenders look at the shape of the file.

They will review:

Credit conduct such as missed payments, unsecured balances, and recent adverse events

Income stability including employment history, probation periods, or variable earnings

Existing commitments that weaken affordability once rent is included

Document quality because incomplete evidence slows decisions and increases caution

A case with straightforward PAYE income and clean credit will often fit a broader lender set than a case relying on bonuses, self-employed income, retained profits, or overseas earnings.

Tip: The cleaner the underwriting story, the less likely the lender is to load pricing for manual complexity.

Mainstream lenders versus specialist lenders

Borrowers often make avoidable mistakes in this area. They assume the biggest bank will give the best answer.

Sometimes it will. Often it will not.

A mainstream lender may treat shared ownership as a niche exception inside a standard residential model. A specialist lender may have dedicated policy, clearer lease requirements, and underwriters who understand the structure well enough to price it more confidently.

That confidence matters. UK shared ownership mortgages often incur a 0.2-0.5% rate premium, yet for high-net-worth borrowers brokers can sometimes negotiate bespoke private bank pricing for 60%+ shares, where the case supports it.

The important point is not that every affluent borrower will achieve that outcome. The point is that lender choice changes the answer.

Property and lease detail

Even an excellent borrower can hit problems if the property itself is awkward.

Lenders usually review:

Lease length and whether it meets policy

Rent review terms on the unsold share

Restrictions on sale or staircasing

Service charges that affect affordability

Provider familiarity if the housing association or scheme is less standard

A shared ownership mortgage is therefore priced at the intersection of borrower strength, property quality, and legal structure. If any one of those is weak, the lender may price defensively or decline the case entirely.

Worked Example Cost Breakdown vs a Standard Mortgage

A buyer who can afford the monthly payment on a full purchase can still fail on deposit. Shared ownership changes that equation, but lenders do not stop at the smaller loan size. They assess whether the whole arrangement remains affordable once rent, service charge, and lease restrictions are layered in.

A direct comparison using the same property value

Take a £250,000 property and compare a standard purchase with a shared ownership purchase at 40%.

Full purchase route

Property value: £250,000

Deposit at 15%: £37,500

Mortgage amount: £212,500

Monthly mortgage payment: £1,121

Shared ownership route at 40%

Full property value: £250,000

Share purchased: 40%

Purchase price of share: £100,000

Deposit at 15% on share: £15,000

Mortgage amount: £85,000

Monthly mortgage payment at 4% over 25 years: £528

The immediate advantage is clear. The deposit hurdle falls by £22,500.

That is exactly why shared ownership works for borrowers who are income-strong but capital-light, including returning expats with UK earnings not yet fully re-established here, and high-net-worth clients whose liquidity is tied up in bonuses, business interests, or investment portfolios. In practice, that lower day-one cash requirement can turn a marginal case into an approvable one.

What the headline saving misses

The lower mortgage payment is only one part of the cost base.

The lender will also consider the rent on the unsold share, service charges, and any other fixed commitments attached to the property. A comparison that ignores those items is not a lending analysis. It is only a partial payment illustration. Some borrowers focus on the reduced mortgage balance and assume the case will price like a low-risk mainstream purchase; however, this often does not occur because from the lender's perspective, shared ownership carries extra structural risk. The security is a partial interest, the lease needs to fit policy, and the exit route can be more controlled if the property has nomination periods or housing association sale restrictions.

How lenders read this scenario

A lender usually likes several features here:

The loan amount is lower, which can improve affordability metrics

The cash deposit required is lower, which helps buyers who have earnings but limited accessible cash

Payment stress testing may be easier to pass on the mortgage element alone

The borrower may preserve reserves after completion, which underwriters often view positively

They will still test the weak points carefully:

Rent and service charge can narrow affordability quickly

Lease terms may fall outside policy even if the borrower is strong

Resale mechanics are less straightforward than on a standard flat or house

Future staircasing may depend on valuation, product availability, and fresh underwriting

For complex borrowers, that last point deserves attention. An expat buying on return to the UK may secure the initial purchase through a specialist lender, then find the remortgage options narrow if income is later split across currencies or overseas contracts. A high-net-worth borrower may qualify comfortably on assets, but still pay more if the lender sees the lease and future exit as less liquid than a standard residential asset.

The practical way to use a worked example

Use the example to test structure, not to decide the case.

Review four numbers before choosing a lender or share size:

Total monthly occupancy cost, including mortgage, rent, and service charge

Cash left after completion, not just minimum deposit paid

How realistic future staircasing is, based on expected income and liquidity

The strongest shared ownership cases are usually the ones where the borrower could afford to buy more later, but chooses not to overstretch at the start. Lenders tend to respond better to that profile than to a file that only works if every affordability assumption holds perfectly.

Navigating the Shared Ownership Mortgage Application

The application process is more layered than a standard purchase. You are not dealing with only one approval gate.

There is usually a scheme or housing association assessment first, followed by lender underwriting. If either side is poorly prepared, the transaction slows down fast.

The file needs to work for two audiences

The housing provider wants to see that you fit the scheme rules and can sustain the arrangement. The lender wants to see that the mortgage and the property meet policy.

Those two assessments overlap, but they are not identical.

A smooth application usually depends on getting three things right early:

Eligibility positioning You need to be clear that shared ownership is appropriate for your circumstances and that you meet the relevant scheme rules.

Document control Missing payslips, inconsistent bank statements, or unclear deposit trails create avoidable friction.

Lender selection The right lender for the lease, income type, and property matters as much as the rate.

Common underwriting pressure points

Some cases become difficult even when the borrower is financially strong.

These include:

Variable income such as bonuses, commissions, or self-employed earnings

Short employment history or recent role changes

Foreign income where exchange risk becomes part of underwriting

Lease or provider complexity if the property falls outside standard policy

Credit blips that a mainstream lender may read more harshly than a specialist

For UK expats, lenders often apply a significant stress test reduction on foreign currency income, such as income paid in USD or AED, to reflect exchange-rate volatility; a limited number of shared ownership lenders also actively cater to non-UK residents.

That does not make borrowing impossible. It means packaging matters more.

Preparing the case properly

A strong application is usually built before the property reservation stage becomes urgent.

Focus on the following:

Income evidence first If your income is unusual, get clarity on what a lender will use before committing.

Explain complexity upfront Overseas employment, family support, or non-standard deposits should be documented clearly.

Review the lease early Do not wait until valuation and legal work are underway to discover a policy issue.

Keep affordability realistic Some borrowers over-focus on maximum borrowing and under-focus on monthly resilience.

Practical takeaway: The strongest shared ownership applications are not the most optimistic. They are the most coherent.

Advanced Strategies to Secure a Lower Interest Rate

Borrowers often treat rate as a market event. It is not. It is partly a market event and partly the result of how your case is presented, structured, and timed.

That distinction matters because it gives you room to improve the outcome.

Improve the deal before you apply

The most effective changes usually happen before a lender sees the file.

A stronger case can come from:

A larger deposit on the purchased share Even a modest improvement can move the case into a more attractive risk band.

Cleaner credit presentation Settle avoidable unsecured balances where sensible, correct reporting errors, and avoid fresh credit applications before submission.

Choosing the right share level The cheapest path on day one is not always the most financeable structure.

Reducing documentary ambiguity Lenders price uncertainty, even when they do not label it that way.

Match the case to the right lender type

Matching the case to the right lender type often helps borrowers gain an edge.

If the case is plain vanilla, a high street option may be fine. If the borrower has overseas income, complex remuneration, substantial assets, or a larger intended share, then lender strategy becomes more nuanced.

Some specialist lenders understand shared ownership well enough to price with more conviction. For high-net-worth borrowers, private banks can sometimes become relevant where the share size is larger and the wider balance sheet is strong.

That does not mean every affluent applicant should head straight to a private bank. Many should not. But when the borrower has investable assets, cross-border income, or a desire for bespoke flexibility, standard sourcing alone may miss viable options.

Think beyond the initial fixed rate

A lower rate that creates problems later is not always the better deal.

Consider:

Early repayment charges if staircasing is likely during the fixed period

Product flexibility if you may remortgage sooner than expected

Lender appetite for future capital raising

How easy the same lender is to work with on shared ownership remortgages

A rate should support your plan, not obstruct it.

If affordability is tight, this guide on ways to improve mortgage affordability is useful because many rate outcomes are won by improving the affordability profile before application rather than arguing about pricing after submission.

What does not work

Three approaches consistently disappoint.

First, applying to the cheapest headline lender without checking lease and policy fit.

Second, assuming a stronger salary alone will override shared ownership complexity.

Third, reserving a property before stress-testing the whole cost structure, especially where rent and service charges are meaningful.

The borrowers who secure the best shared ownership mortgage rates usually do the unglamorous work early. They tighten the case, choose the structure carefully, and avoid lenders whose policy was never a true fit.

The Long-Term View Remortgaging and Staircasing

Shared ownership only works well when the long-term path is considered at the outset. The first mortgage is important, but it is not the whole strategy.

For many buyers, the primary objective is either to improve the terms later, buy further shares over time, or reach full ownership if the lease allows.

Staircasing changes the risk profile

Staircasing means buying additional shares in the property after your initial purchase.

That can be attractive for obvious reasons. You increase your ownership stake and reduce the unsold share over time. In some cases, the long-term destination is full ownership. In others, the borrower wants a larger share and a more balanced monthly structure.

The strategic question is timing.

Buying more shares can make sense when your income has strengthened, your property has performed well, or a remortgage allows a better funding structure. It can make less sense when early repayment charges are active or when the current lender is poorly suited to the next phase.

Remortgaging a shared ownership property

Remortgaging can serve more than one purpose.

Sometimes it is about securing a better rate on the existing shared ownership mortgage. Sometimes it is about raising funds to staircase. Sometimes it is about restructuring onto a more suitable lender before a future move.

The practical issues usually include:

A fresh valuation to establish current market value

Review of the lease and housing provider requirements

Assessment of any early repayment charges

Affordability testing based on the revised structure

These cases need careful timing. A borrower may save money by remortgaging, then lose flexibility if the new product creates restrictive penalties just before they want to buy more shares.

For borrowers considering that route, this page on remortgages is a useful reference point for the mechanics involved.

The endgame matters

Once a borrower staircases to full ownership, the property may become eligible for a standard residential remortgage rather than a shared ownership product, subject to the lease and scheme terms.

That can be significant. The borrower may remove the rent element entirely and access a broader mainstream lender pool.

Key takeaway: The best shared ownership mortgage is often the one that keeps your future remortgage and staircasing options open, not the one with the lowest day-one payment.

Frequently Asked Questions

Are shared ownership mortgage rates always higher than standard residential rates

Not always in a meaningful practical sense, but they often come with some premium because the lender is funding a more complex structure. The key issue is not only the rate. It is whether the overall arrangement improves your entry cost and remains workable over time.

Can I get a shared ownership mortgage as a UK expat

Sometimes, yes, but lender choice is narrow. For UK expats, lenders often reduce foreign currency income for stress testing, and a limited number of shared ownership lenders also actively cater to non-UK residents. That means foreign income quality, currency, documentation, and residency status all need to be presented very carefully.

Is a bigger share always better for mortgage pricing

Not necessarily. A bigger share can help with lender comfort in some cases, especially for stronger borrowers, but it also creates a larger loan requirement. The right answer depends on how the lender views affordability, the rent burden on the unsold share, and your longer-term plan.

Can I remortgage before I staircase

Yes, if the lender and property fit policy and the existing mortgage terms allow it. The timing matters. Some borrowers should remortgage first and staircase later. Others should combine the two steps. Early repayment charges and valuation timing often drive that decision.

What tends to go wrong in shared ownership applications

The most common issues are not mysterious. Borrowers underestimate the importance of lease review, choose a lender on headline rate rather than policy fit, or submit a case with weak income evidence. Foreign income, variable pay, and unusual property terms need extra care.

Is shared ownership a good idea for high-net-worth borrowers

In some cases, yes. A high-net-worth borrower may use the structure selectively, particularly where liquidity, tax planning, or cross-border income considerations matter more than maximising initial ownership. The right strategy depends on the wider balance sheet, not just the property purchase in isolation.

📞 Want Help Navigating Today’s Market?

Book a free strategy call with one of our mortgage specialists. We’ll help you find the smartest way forward, whatever rates do next.

Tailored advice for individuals, businesses and professional advisers seeking sophisticated financial solutions.

At Willow Private Finance, we understand that every client has different ambitions, financial circumstances and long-term objectives. Whether you are purchasing property, refinancing existing borrowing, protecting your family or business, or looking to unlock wealth through specialist lending, we build solutions around your individual needs rather than forcing you into standard products.

As an independent, whole-of-market brokerage, we provide access to residential mortgages, buy-to-let finance, bridging loans, development finance, commercial lending, private banking and Lombard lending facilities, alongside a comprehensive range of personal and business protection solutions. Our expertise extends to UK and international clients, high-net-worth individuals, company directors, investors, expatriates and borrowers with complex financial structures.

By combining deep technical expertise with relationships across mainstream lenders, specialist lenders and private banks, we help clients secure funding, structure borrowing efficiently and protect the assets, income and people that matter most. Whatever stage of your financial journey you are at, our team is here to provide clear, strategic advice that delivers confidence and long-term value.

From mortgages and private banking to Lombard lending, business finance and protection planning, Willow Private Finance delivers bespoke solutions for even the most complex financial requirements.

Wesley Ranger is a senior finance professional with over 20 years’ experience in the UK mortgage and specialist lending markets. As a director at Willow Private Finance, he has advised extensively on affordable housing schemes, including shared ownership and part-buy, part-rent structures.

His expertise includes lender underwriting for shared ownership mortgages, affordability modelling that incorporates rent and mortgage payments, and navigating housing association requirements. Wesley has worked with a wide range of clients, particularly first-time buyers and those accessing the property market through alternative ownership structures.

He has a detailed understanding of how lenders assess shared ownership applications, including deposit requirements, income thresholds, and long-term affordability considerations. His experience spans both high street lenders and specialist providers, giving him a comprehensive, whole-of-market perspective.

Wesley regularly advises on structuring applications for shared ownership, ensuring that borrowers understand both the lending and contractual elements involved in these arrangements.

Important Notice

This article is for general information purposes only and does not constitute personal financial advice, tax advice, or legal advice. Mortgage availability, criteria, and rates depend on individual circumstances and may change at any time.

Shared ownership mortgages involve purchasing a percentage of a property while paying rent on the remaining share, typically to a housing association. Affordability assessments consider both mortgage repayments and rental commitments, and eligibility is subject to scheme criteria and lender requirements.

Examples, scenarios, and market commentary are illustrative only and do not represent any specific lender’s current policy or a guarantee of outcome. Borrowers should carefully consider the long-term financial implications of shared ownership, including rent increases and staircasing costs.

Your home may be repossessed if you do not keep up repayments on a mortgage or any debt secured against it.

Willow Private Finance Ltd is authorised and regulated by the Financial Conduct Authority (FCA No. 588422). Registered in England and Wales.

HSBC's reported pullback from parts of the private credit market highlights why developers, family offices and complex borrowers need specialist funding advice.

Gulf buyers from the UAE, Saudi Arabia and Qatar are returning to London's prime property market. Discover why early finance preparation is becoming increasingly important.

Family offices are increasingly outsourcing specialist expertise as portfolios become more complex. Discover why specialist property finance partners are becoming essential for wealth managers, trustees and private client advisers.

Knight Frank's latest research examines how rental reform and future tax risks are reshaping the prime rental market and why landlords should review their finance strategy.

Discover what the Bank of England's 2026 Financial Stability Report means for high-value borrowers, refinancing, private banking and specialist property finance.

New concerns over mansion tax valuations mean owners of £2m+ homes should review property finance, Lombard lending and wealth planning before the High Value Council Tax Surcharge begins in 2028.

NatWest has completed its £2.7bn acquisition of Evelyn Partners, creating the UK's largest private banking and wealth management business. Discover why specialist property finance partnerships matter more than ever.

Financial Times reports growing use of Lombard lending for property purchases as affluent investors borrow against portfolios instead of selling assets.