Free Consultation. Free Finance Assessment. No Obligation.

At Willow Private Finance, there isno charge to speak to one of our specialist advisorsandno charge for us to assess your requirements and identify suitable finance solutions.

We'll take the time to understand your circumstances, review your objectives and explore the options available to you before you decide whether you want to proceed.

Should you wish to move forward with a recommended solution,any applicable fees will be clearly explained and agreed in advance, ensuring complete transparency from the outset.

Once instructed, we'll manage the process from application through to completion, liaising with lenders, solicitors, valuers and other professionals involved in the transaction to help secure the funding you require.

A common 2026 scenario looks like this. You own a good property, you locked into a strong fixed rate at the right time, and now you need capital. The money may be for works on the house, a tax bill, debt consolidation, a business injection, or a deposit for another purchase.

The problem is not always affordability. It is structure.

If your existing first mortgage is cheap and carries painful early repayment charges, replacing it just to raise extra money can be an expensive move. In those cases, a second charge mortgage often enters the conversation quickly. For the right borrower, it is not a workaround. It is a deliberate financing choice.

For accountants, solicitors, wealth advisers and experienced borrowers, the central question is rarely only what is second charge mortgage. The better question is when a second charge is strategically better than remortgaging, a further advance, unsecured borrowing, or short-term finance.

An Introduction to Second Charge Mortgages

An expat with a low fixed first mortgage, a portfolio landlord protecting existing facilities across several properties, and a high-net-worth borrower who wants liquidity without reopening private banking arrangements can all arrive at the same answer. A second charge mortgage.

A second charge mortgage is a secured loan against a property that already has a first mortgage. The original mortgage remains in place, and the new lender registers a second legal charge over the property. In practice, that means the borrower raises capital without replacing the first charge facility.

That structure is what makes the product useful. In the right case, it preserves an attractive first mortgage, avoids unnecessary early repayment charges, and keeps an existing debt arrangement intact. For complex borrowers, those points often matter more than the headline rate on the new borrowing.

Second charge lending remains specialist rather than mainstream. The reason is straightforward. Cases are often more technical, the source of income may be less standard, the purpose of funds may need tighter justification, and lender appetite varies from one profile to another. A salaried homeowner with clean payslips is one type of case. An expat paid in multiple currencies, a landlord with layered SPV and personal borrowing, or a wealthy client with asset-rich but income-light structuring is another.

That is where a specialist broker adds real value. The job is not only to find a lender willing to take a second charge. It is to place the case with a lender whose criteria fit the borrower’s actual profile, income treatment, property type, and intended use of funds. The Financial Ombudsman Service has also highlighted second charge complaints involving suitability and advice failures, which is a useful reminder that product selection and explanation need to be handled carefully from the outset.

Why This Matters in the Current Market

In the 2026 UK property market, borrowers are still dealing with the legacy of higher rates, stricter underwriting, and closer scrutiny of complex income. Many first mortgages written in earlier years remain worth keeping. Breaking those arrangements just to raise capital can be commercially weak.

Second charges have become more strategic for that reason. They are often used because the structure fits better, not because the borrower has run out of options.

The strongest cases usually share three features:

There is sufficient equity in the property

The first mortgage has value worth preserving, whether because of rate, term, flexibility, or penalties

The borrowing purpose stands up under underwriting, particularly where the client is consolidating debt, funding works, injecting business capital, or raising liquidity for a purchase

For experienced borrowers and their advisers, the question is rarely just what a second charge mortgage is. A key question is whether it is the cleanest way to raise capital without disturbing a first charge that should be left alone.

The Mechanics of a Second Charge Mortgage

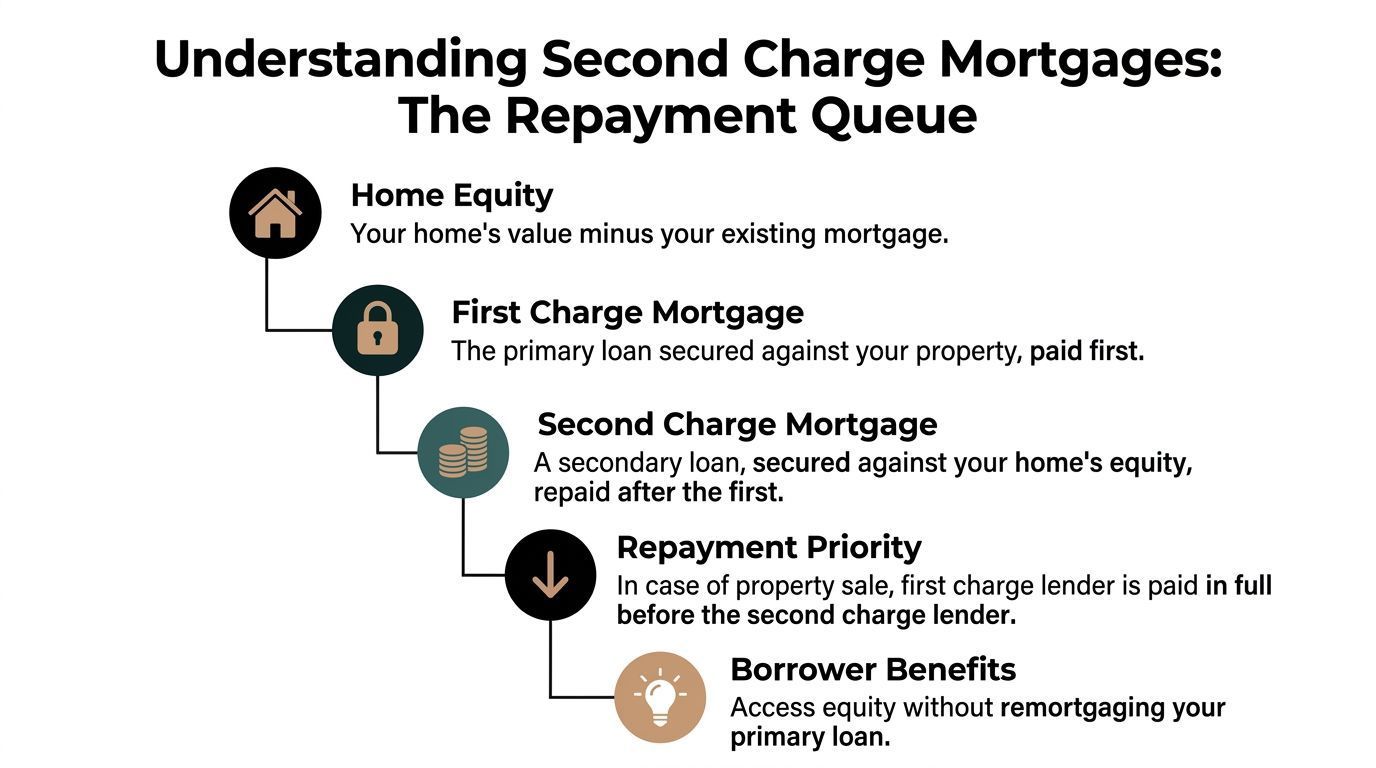

The cleanest way to understand a second charge is to think in terms of a repayment queue.

The first mortgage lender stands at the front of that queue. The second charge lender stands behind them. If the property is sold following default, the first lender is repaid first. The second lender is repaid only after the first charge debt has been cleared.

That legal priority is why second charge lending is priced differently. A second charge mortgage is a secured loan against the equity in a property that already has a first charge mortgage, and the second lender ranks behind the first in repayment priority. Lenders typically advance 60-85% LTV on the available equity, while total borrowing across first and second charges rarely exceeds 75-85% combined LTV. That subordinate position also means higher interest rates, with the cited guide noting pricing typically 4-8% above first charges, for example 7-12% APR versus 4-6% base rates in 2023-2025 UK data.

How equity is assessed

The lender starts with the property value and subtracts the balance outstanding on the first mortgage. What remains is the equity position.

That does not mean the lender will advance against all of it. They will apply their own loan-to-value limits and affordability model. They will also look at the property type, borrower profile, and intended use of funds.

Why combined LTV matters

The combined position matters more than many borrowers realise. A second charge lender considers factors beyond the size of their own loan. They are also judging the total debt secured on the property once both loans are in place.

In practice, this means a client with a strong income but thin remaining equity may still find terms restricted. By contrast, a borrower with healthy equity and a straightforward exit can often access better options even if the case has complexity elsewhere.

The legal and underwriting framework

Second charges sit inside a regulated environment. That means paperwork, affordability assessment, lender checks and legal registration all matter.

Expect scrutiny in these areas:

Property security. The lender wants a property they can lend against with confidence.

Repayment capacity. Affordability is central, even where the client has substantial assets.

Use of funds. Lenders are more comfortable where the purpose is coherent and documented.

First lender position. The existing first mortgage remains senior and must be factored into the structure.

In second charge lending, strong cases are not just affordable. They are explainable.

Common Strategic Uses for a Second Charge Loan

A second charge starts to make sense when the borrowing need is clear, the first mortgage is worth preserving, and the client wants capital without disturbing the wider structure.

In the UK 2026 market, that often applies to borrowers whose affairs do not fit a high street template. Expats with sterling assets but overseas income, portfolio landlords managing multiple facilities, and high-net-worth clients with strong balance sheets but irregular taxable income often use second charges as a planning tool rather than a last resort. The product itself is straightforward. Matching the case to the right lender is usually the harder part.

Debt consolidation

Debt consolidation remains a common use, but it only works well when the underlying issue is contained.

A borrower may have unsecured balances across cards, loans, or short-term facilities while also holding substantial equity and an attractive first-charge rate. A second charge can roll those liabilities into one secured loan and leave the first mortgage untouched. That can improve monthly cash flow and simplify the debt position.

The trade-off is obvious. Unsecured debt becomes borrowing against the home.

That is why a proper broker review matters. I would want to see whether the client is fixing a temporary pressure point, such as a disrupted bonus cycle or business cash extraction, or stretching an already weak position. Borrowers considering this route should review the implications of debt consolidation with property finance before securing short-term debt against a property.

Home improvements

Home improvements are often one of the cleaner second charge cases because the purpose is tangible and the funds can be evidenced.

Typical examples include extensions, major refurbishments, reconfiguration, and energy-efficiency works. For a client sitting on a low fixed first mortgage, a second charge can be a more efficient route than replacing the whole facility just to raise capital for works.

At the prime and super-prime end, the point is rarely just the build cost. Timing matters as much. A high-net-worth borrower may want to fund works now, preserve liquidity for tax or investment purposes, and refinance later once the property and income profile present better. Lenders will still want a sensible cost schedule, contractor detail in larger cases, and a believable repayment strategy.

Raising capital for a wider strategy

The more interesting cases are usually strategic rather than domestic.

A second charge can be used to release capital for a deposit on another purchase, inject funds into a trading business, settle a tax liability without liquidating investments, or bridge a timing gap before a sale, refinance, carried interest payment, or deferred remuneration event. For expats and entrepreneurial clients, that flexibility can be more valuable than headline rate.

Portfolio landlords use second charges in a similar way. A landlord may want to raise funds against a main residence rather than disturb a portfolio structure that already has lender concentration, product deadlines, or property-level restrictions. In the right case, that keeps existing buy-to-let debt in place and creates room to act quickly on an acquisition or asset management opportunity.

The weakness in these cases is not the purpose. It is lender fit. Some lenders are comfortable with complex income and asset-backed borrowers. Others are not. A specialist broker earns their fee by knowing which lenders will accept overseas earnings, retained profits, layered property exposure, trust income, or non-standard security without wasting weeks on the wrong credit appetite.

What tends not to work well

Second charges tend to struggle where the use of funds is vague, the repayment plan depends on optimism, or the borrower is trying to solve a structural affordability problem with more secured debt.

Lenders can accept complexity. They are much less comfortable with inconsistency.

The strongest cases are clear on three points. Why the money is needed, why a second charge is the right structure, and how the debt will remain affordable under scrutiny.

Comparing Second Charge Mortgages and Key Alternatives

No borrower should look at a second charge in isolation. The right question is whether it is better than the alternatives available to you at the same moment.

Second charge versus remortgaging

Remortgaging replaces the first mortgage entirely. Sometimes that is the obvious answer. If your current product is ending, the pricing is still competitive, and the new mortgage can deliver the capital you need cleanly, remortgaging may be simpler.

It becomes less attractive when the existing mortgage is worth preserving.

That may be because:

The rate is unusually good

The fixed period still has time left

Early repayment charges would make the switch expensive

The existing lender’s terms are otherwise worth keeping

A second charge can sit behind that first mortgage and leave it untouched. The trade-off is that second charge pricing is usually higher than first charge pricing, as covered earlier. So the analysis is never just “which rate is lower”. It is “what is the total cost of disturbing the current structure versus adding a second facility”.

Second charge versus further advance

A further advance comes from your existing mortgage lender. If they are willing to provide it, this can be a neat route because you are dealing with the current bank.

But many borrowers hit one of four issues. The lender may decline the purpose, cap the loan, price it unattractively, or move too slowly for the practical deadline.

A second charge often becomes useful where the main lender says no, says not enough, or says yes on terms that do not suit the case. This is especially common with complex incomes, unusual property types, portfolio exposure, or foreign income.

Unsecured lending can be sensible for smaller sums and shorter horizons. It avoids charging the property and may be operationally simpler.

The limits are obvious. Large unsecured borrowing becomes harder to justify, pricing can be steep, and monthly payments can be demanding. A second charge may produce a more workable structure for a larger requirement because it spreads repayment over a longer mortgage-style term and uses property equity as security.

That does not make it safer. It makes it different. The house is now part of the credit decision.

Second charge versus bridging finance

Bridging finance solves a different problem.

Bridging is usually the right tool where the borrower needs short-term capital for speed, chain break, auction purchase, refurbishment before refinance, or another time-critical event with a defined exit. It is not designed to behave like a long-term mortgage.

A second charge is more suitable where the requirement is medium- to long-term and the borrower wants regular monthly servicing rather than a short-term exit-driven facility.

A practical decision filter

Ask these questions in order:

Do I want to preserve my current first mortgage?

Is my borrowing need temporary, short-term, or ongoing?

Will my existing lender support the case?

Does unsecured borrowing solve the need without charging the property?

Is the use of funds clear enough to support specialist underwriting?

The lowest headline rate is not always the cheapest strategy. Structure, penalties, flexibility and timing decide that.

Lender Criteria and Borrower Eligibility

Eligibility is where many online explanations become too simplistic. A second charge lender is not only asking whether you own a property with equity. They are asking whether the whole case stands up under underwriting.

What lenders review first

The first screen is usually built around three things:

Income and affordability

Credit profile

Available equity

For employed borrowers, the income side is straightforward. For self-employed clients, portfolio landlords, and directors drawing income in different ways, the analysis gets more technical.

The same applies to high-net-worth applicants. Wealth helps, but it does not replace underwriting. Lenders still want a coherent servicing story.

Expats and international buyers

For expats and international buyers, criteria can move in these circumstances.

For expats and international buyers, second charge lending can involve more checks around residency, foreign income verification, source of wealth, and cross-border compliance. One cited source states that second charge lending volumes among non-UK residents rose 18% in Q4 2025, while lenders often apply 60-70% LTV caps for expats and may charge 2-3% higher rates because of compliance complexity.

That does not mean expat cases are unworkable. It means they need cleaner packaging. Foreign currency income, overseas tax documentation, and multi-jurisdictional asset structures all require more deliberate preparation.

Portfolio landlords and complex borrowers

Portfolio landlords assume a second charge will be judged only on the subject property. In reality, lenders may also take a view on the wider portfolio, existing borrowing, rental coverage, and background conduct.

High-net-worth clients run into a different issue. Their affordability may be obvious economically but awkward on paper. Trust distributions, retained profits, foreign assets, carried interest, and irregular income streams are not easy fits for standard underwriting templates.

That is why case presentation matters. A lender-friendly summary of income, assets, liabilities and purpose can change how a case is received.

A clear borrowing purpose with supporting documents

A sensible equity position after the new loan completes

Evidence of stable income, even if that income is structured unusually

A credible explanation for any historic credit issues

Clean paperwork from the outset

Specialist lending is often less about fitting a rigid box and more about presenting a convincing case within lender policy.

Understanding the Full Costs and Risks Involved

The rate matters, but it is not the whole cost.

A second charge can also involve lender fees, valuation costs, legal costs, and broker fees. The exact shape varies by lender and case complexity. On a straightforward residential file, the process may be clean. On an expat, trust-held, or higher-value transaction, the surrounding costs and documentation can be more involved.

You also need to think about timing cost. If the alternative is to redeem a first mortgage early, the right comparison is not just second charge pricing versus first charge pricing. It is second charge pricing versus the total cost of breaking the existing deal, including any penalties and downstream restructuring effects. Borrowers reviewing this point should understand early repayment charges ERCs in 2025 timing your switch and saving thousands.

The core risk

The most important risk is straightforward. Your home, or other secured property, is at risk if payments are not maintained.

That risk is underappreciated when the loan is used to tidy up unsecured debt or create liquidity for another purpose. A second charge can improve financial control, but only if the new arrangement is affordable and disciplined.

A sensible way to assess it

Before proceeding, test the case under pressure:

If income drops, do payments still work?

If the property value softens, does the structure still make sense?

If the planned use of funds underperforms, is the debt still serviceable?

That is the true risk analysis. Not whether the product sounds flexible, but whether the borrower can live with the structure in a less forgiving year.

How to Secure the Right Second Charge Finance

The second charge market rewards case preparation. It does not reward vague enquiries sent to a handful of lenders in the hope something sticks.

The right process starts with diagnosis. Is a second charge the right solution, or just the first one the borrower has heard about? That means reviewing the first mortgage, checking whether a further advance is viable, testing remortgage economics, and understanding the exact purpose of funds.

Why specialist broking matters

Second charge lending is fragmented. Criteria differ. Appetite differs. Documentation standards differ.

That is why many complex borrowers use a specialist broker rather than approaching lenders blind. A broker can match the case to lender appetite, present foreign income properly, frame a portfolio case coherently, and identify where private bank or specialist structured options may sit outside the standard high-street route.

One option in the market is Willow Private Finance, which arranges mortgages and specialist finance across standard and complex cases.

The practical next step

Come to the discussion with documents, not a vague headline idea.

Have ready:

Mortgage statements

Proof of income

A schedule of debts or assets where relevant

A clear explanation of the funds required and why

Any timing pressure that affects lender choice

That produces better lender selection and fewer surprises later in the process.

Residential Mortgages

Is A Second Charge Mortgage Really Your Best Option?

As this guide explains, choosing between a second charge mortgage, a remortgage, a further advance or even bridging finance is rarely as simple as comparing interest rates. The right solution depends on your existing mortgage, the purpose of the borrowing, your income structure and which lenders are prepared to support your circumstances.

Visit our Residential Mortgages Hub

to explore expert guides covering remortgaging, capital raising, interest-only mortgages, complex income, expat borrowing, bridging finance and other specialist lending solutions. You'll also find real client case studies showing how carefully structured advice can help borrowers preserve low-rate mortgages while accessing the capital they need.

Frequently Asked Questions About Second Charge Mortgages

Can you get a second charge mortgage on a buy-to-let property

Yes, in many cases you can. The lender will assess the property, the existing mortgage position, the equity available, and the wider background of the landlord. If the borrower owns multiple properties, the lender may also want to understand the overall portfolio rather than looking only at the single asset.

Rental income can form part of the underwriting picture, but the exact method varies by lender and by whether the case is regulated or unregulated.

What happens if you sell the property before the second charge is repaid

The second charge does not disappear because the property is being sold. On completion, the legal charges must be redeemed in order of priority. The first charge lender is paid first. The second charge lender is paid after that from the sale proceeds.

If the borrower is planning a sale in the near term, this should be discussed at the outset. The wrong product can become expensive if the intended holding period is short.

How long does a second charge mortgage take

There is no single timeline.

Straightforward cases can move efficiently. Complex cases involving foreign income, layered company structures, unusual properties, or more than one legal jurisdiction can take longer because the underwriting and document review are heavier. The practical answer is to start early and package the case well.

Is a second charge bad for your credit profile?

Not necessarily. It is another debt commitment, so lenders will see it as part of your overall obligations. The impact depends on the wider profile, the affordability position, and whether payments are maintained on time.

Is what is second charge mortgage the same as having two normal mortgages

No. A second charge mortgage is a second loan secured on the same property behind the first charge lender. That is different from having separate mortgages on separate properties.

📞 Want Help Navigating Today’s Market?

Book a free strategy call with one of our mortgage specialists. We’ll help you find the smartest way forward, whatever rates do next.

Tailored advice for individuals, businesses and professional advisers seeking sophisticated financial solutions.

At Willow Private Finance, we understand that every client has different ambitions, financial circumstances and long-term objectives. Whether you are purchasing property, refinancing existing borrowing, protecting your family or business, or looking to unlock wealth through specialist lending, we build solutions around your individual needs rather than forcing you into standard products.

As an independent, whole-of-market brokerage, we provide access to residential mortgages, buy-to-let finance, bridging loans, development finance, commercial lending, private banking and Lombard lending facilities, alongside a comprehensive range of personal and business protection solutions. Our expertise extends to UK and international clients, high-net-worth individuals, company directors, investors, expatriates and borrowers with complex financial structures.

By combining deep technical expertise with relationships across mainstream lenders, specialist lenders and private banks, we help clients secure funding, structure borrowing efficiently and protect the assets, income and people that matter most. Whatever stage of your financial journey you are at, our team is here to provide clear, strategic advice that delivers confidence and long-term value.

From mortgages and private banking to Lombard lending, business finance and protection planning, Willow Private Finance delivers bespoke solutions for even the most complex financial requirements.

The UK property finance market moves quickly. Mortgage rates change, lenders update criteria, specialist products launch and market conditions evolve every week. Keeping on top of these developments can be difficult, whether you're a homeowner, landlord, developer, investor or professional adviser.

Our free weekly briefing brings together the stories that matter most, alongside expert commentary from Willow Private Finance, helping you stay informed without having to monitor multiple news sources.

Weekly summary of the UK's biggest property finance stories

Residential, buy-to-let, bridging and development finance updates

Private banking, Lombard lending and HNW market insights

UK expat and overseas buyer developments

Market commentary from experienced finance specialists

Free to subscribe with no obligation

Delivered every Week.

Join a growing community of homeowners, investors, developers, accountants, solicitors, estate agents and wealth advisers receiving Willow's weekly Property Finance Briefing.

About the Author

Wesley Ranger is a senior finance professional with over 20 years’ experience in the UK mortgage and specialist lending markets. As a director at Willow Private Finance, he has extensive experience advising on secured lending, including second charge mortgages and complex refinancing strategies.

His expertise includes structuring borrowing against existing property equity, assessing lender underwriting for layered debt, and navigating cases where traditional remortgaging may not be suitable. Wesley has worked with homeowners, landlords, and high-net-worth individuals to structure second charge lending across a wide range of financial scenarios.

He has a detailed understanding of how lenders assess affordability, credit profile, and security position when a second charge is introduced. His experience spans specialist lenders and private funding sources, providing a comprehensive, whole-of-market perspective on secured borrowing.

Wesley regularly advises on debt restructuring, capital raising, and strategic use of property equity, ensuring that borrowing aligns with both lender expectations and long-term financial planning.

Important Notice

This article is for general information purposes only and does not constitute personal financial advice, tax advice, or legal advice. Mortgage availability, criteria, and rates depend on individual circumstances and may change at any time.

Second charge mortgages are secured loans taken against a property that already has an existing mortgage. They involve additional risk, as the lender holds a secondary claim on the property, and affordability, credit profile, and existing borrowing will be assessed. Not all borrowers will be eligible, and terms may vary significantly between lenders.

Examples, scenarios, and market commentary are illustrative only and do not represent any specific lender’s current policy or a guarantee of outcome. Borrowers should carefully consider the risks associated with additional secured borrowing, particularly where multiple loans are secured against the same property.

Your home may be repossessed if you do not keep up repayments on a mortgage or any debt secured against it.

Willow Private Finance Ltd is authorised and regulated by the Financial Conduct Authority (FCA No. 588422). Registered in England and Wales.

HSBC's reported pullback from parts of the private credit market highlights why developers, family offices and complex borrowers need specialist funding advice.

Gulf buyers from the UAE, Saudi Arabia and Qatar are returning to London's prime property market. Discover why early finance preparation is becoming increasingly important.

Family offices are increasingly outsourcing specialist expertise as portfolios become more complex. Discover why specialist property finance partners are becoming essential for wealth managers, trustees and private client advisers.

Knight Frank's latest research examines how rental reform and future tax risks are reshaping the prime rental market and why landlords should review their finance strategy.

Discover what the Bank of England's 2026 Financial Stability Report means for high-value borrowers, refinancing, private banking and specialist property finance.

New concerns over mansion tax valuations mean owners of £2m+ homes should review property finance, Lombard lending and wealth planning before the High Value Council Tax Surcharge begins in 2028.

NatWest has completed its £2.7bn acquisition of Evelyn Partners, creating the UK's largest private banking and wealth management business. Discover why specialist property finance partnerships matter more than ever.

Financial Times reports growing use of Lombard lending for property purchases as affluent investors borrow against portfolios instead of selling assets.