Free Consultation. Free Finance Assessment. No Obligation.

At Willow Private Finance, there isno charge to speak to one of our specialist advisorsandno charge for us to assess your requirements and identify suitable finance solutions.

We'll take the time to understand your circumstances, review your objectives and explore the options available to you before you decide whether you want to proceed.

Should you wish to move forward with a recommended solution,any applicable fees will be clearly explained and agreed in advance, ensuring complete transparency from the outset.

Once instructed, we'll manage the process from application through to completion, liaising with lenders, solicitors, valuers and other professionals involved in the transaction to help secure the funding you require.

First Time Buyer Mortgage Brokers: Your Guide for 2026

Buying your first home in the UK can feel oddly contradictory. You may have done the sensible things, built a deposit, kept your credit tidy, researched rates, and still feel as though you are trying to decode a system that was not designed for beginners.

That feeling is not a lack of preparation. It is a realistic response to a market with tighter affordability rules, a wider spread of lender criteria, and more moving parts than most buyers expect at the outset. A first-time buyer mortgage is not just about finding a rate. It involves fitting your income, deposit, documents, timing, and property choice into a lender’s underwriting model without making expensive mistakes on the way.

First time buyer mortgage brokers earn their place in this context. The best brokers do far more than compare products. They assess borrowing power properly, identify avoidable risks early, structure the application around lender criteria, and manage the process across estate agents, solicitors, underwriters and valuers. For buyers with straightforward PAYE income, that can save time and stress. For buyers with non-standard income, gifted deposits, overseas earnings, recent job moves, self-employment, or scheme-based purchases, it can be the difference between a clean approval and a frustrating dead end.

Introduction The First-Time Buyer Challenge in 2026

A common starting point looks like this. You have a deposit, perhaps with help from family or years of disciplined saving. You open a few lender calculators, get three different answers, then discover that the headline number is not the same as a usable lending decision. One lender seems comfortable with your bonus income. Another ignores part of it. A third likes your salary but dislikes the building you want to buy.

This is not a niche problem. In the UK, first-time buyers made up just 26% of all house purchases in 2024, the lowest proportion since records began in 1953, while specialist mortgage brokers assisted 90% of first-time buyers in securing mortgages in 2024, up from 85% in 2020, according to theONS house price index release. That tells you two things at once. Buying has become harder, and buyers increasingly need specialist help to get through it.

The pressure shows up in practical ways:

Affordability is tighter: Lenders do not just ask what you earn. They test what you can still afford if circumstances change.

Deposit sourcing matters: A gifted deposit, bonus income, commission, or foreign currency salary can all be acceptable, but only if presented properly.

Property choice affects lending: Flats above commercial units, short leases, ex-local authority homes, and some new-builds can narrow lender choice quickly.

A good broker acts less like a middleman and more like a strategist. They help you understand what will work before you spend money on surveys, legal work, and mortgage application fees.

The first-time buyer mistake is not asking for advice too early. It is waiting until an offer is accepted, then discovering the lender sees your case very differently from the online calculator.

What a First-Time Buyer Mortgage Broker Does

A broker’s work starts well before any application is submitted. Value is often added at that early stage; weak points are identified and fixed there before a lender sees the case.

Adviser, not just rate finder

A proper fact-find goes deeper than income and deposit. The broker will look at your employment structure, regular outgoings, existing credit, bank conduct, source of deposit, target property type, and timing.

That matters because lenders assess risk differently. One may be comfortable with probationary employment. Another may not. One may use retained profit for a company director in a certain way. Another may focus only on salary and dividends.

The best early advice often sounds unglamorous but saves deals:

Wait before applying: If your last three months’ bank statements show avoidable strain, a short pause may strengthen the case.

Restructure the deposit evidence: Gifted deposits are common, but documentation must be clear and consistent.

Choose the property with financing in mind: A cheap flat is not a bargain if it cuts the lender pool dramatically.

Analyst of lender criteria

Most first-time buyers assume mortgage underwriting is mostly numeric. In practice, it is numeric plus policy. The numbers may fit, but the lender’s internal rules still decide whether the case is acceptable.

A broker translates your situation into lender language. That means identifying who is likely to accept your income mix, your deposit source, and the property. It also means avoiding lenders whose criteria create a predictable rejection.

Project manager from application to completion

Once the lender is chosen, the broker’s role becomes operational. This is the part many buyers underestimate.

A broker typically helps with:

Document collection so the file is complete and consistent.

Submission packaging so the underwriter sees a coherent case.

Lender queries which need fast, accurate answers.

Coordination with solicitors and agents to keep the transaction moving.

Offer tracking so delays are spotted early.

That is very different from using a comparison site and then managing the rest yourself. If you want to understand why timing matters so much, early advice from a first-time buyer broker explains the advantage of getting your structure right before you start bidding.

The Strategic Benefits of Using a Specialist Broker

The value of specialist advice is usually felt in three places: Money, Time, Outcome.

Better overall cost, not just a lower headline rate

First-time buyers often focus on the interest rate because it is the easiest figure to compare. It is not always the most important one. A thorough comparison includes arrangement fees, valuation costs, incentives, revert rate risk, cashback, and whether the product still suits you if your plans change. A lower rate with a heavy fee structure can be worse value than a slightly higher rate with lower upfront cost.

According to the Which? mortgages guidance pages, first-time buyers who use a mortgage broker save an average of £1,200 on mortgage fees and related costs compared with applying directly, due to better product access and negotiation.

That number matters because first-time buyers usually have competing demands on cash. Legal fees, moving costs, furnishing, and contingency funds all land at once.

Less wasted time

The time saving is not only about outsourcing paperwork. It is about avoiding false starts.

Going direct often creates duplication. You explain your case to one lender, then another, then another. Each has different questions, different document standards, and different tolerances. A broker compresses that process by filtering the market before the application begins.

Specialist brokers also know where applications tend to stall. Common pressure points include:

Bank statement reviews

Gifted deposit checks

Bonus or commission evidence

Property valuation concerns

Solicitor enquiries on title or lease terms

Stronger chance of a clean approval

This is the part borrowers tend to appreciate most after the fact; a strong broker reduces the odds of avoidable friction.

That does not mean every case is easy. It means the right lender is chosen for the actual case, not the idealised version of it. If your income is mixed, your deposit comes partly from family, or your file needs explanation, packaging matters.

Good brokerage work is often invisible to the client. The case looks smooth because the difficult parts were handled before they became problems.

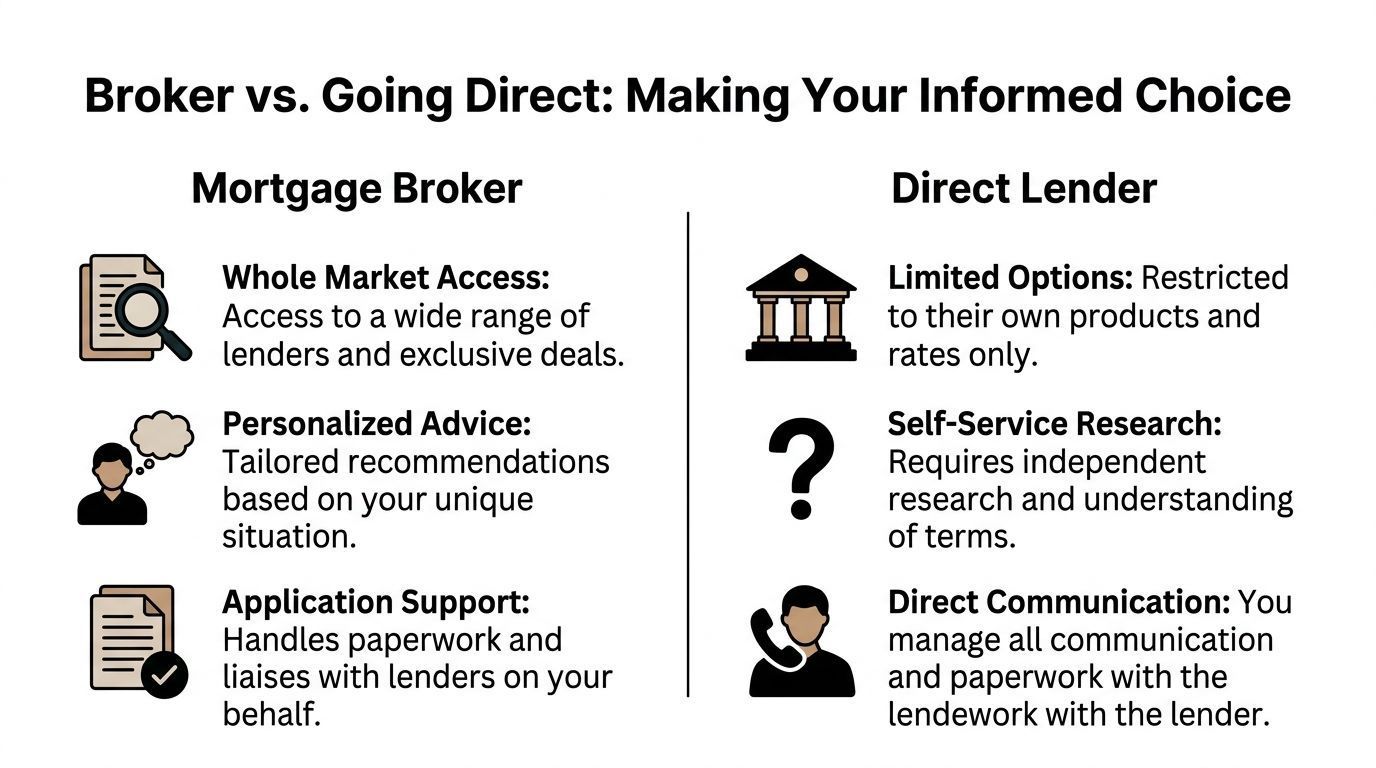

Broker vs Going Direct A Clear Comparison

There is nothing wrong with going direct to a lender. For some buyers with very simple income, a strong deposit, and a standard property, it can work perfectly well. The issue is not whether it can work. The issue is what you give up by limiting yourself to one lender at a time.

What going direct gives you

The appeal is easy to understand. You deal with a familiar brand, speak to that lender’s own team, and may feel you are removing a layer from the process.

That can suit buyers who already know the lender is a strong fit and whose circumstances are highly conventional.

But there are trade-offs.

You only see that lender’s criteria and products

You carry the research burden yourself

You manage the application logistics

You may only discover policy issues after time has been lost

A direct lender can explain its own products. However, it cannot advise you that another lender would treat your income, property, or deposit more favourably.

What using a broker changes

A broker gives you a wider decision framework. Instead of asking, “Will this lender accept me?”, the better question becomes, “Which lender is best suited to this case?”

That shift matters most when any of the following apply:

Self-employed income

Recent change of job

Probation period

Gifted deposit

Debt that looks manageable in life but awkward on paper

Unusual property construction or tenure

Overseas income or residency complexity

The broker’s value is not just selection. It is sequencing. The order in which things are done can protect your options. For example, securing the right agreement in principle before offering, clarifying gift documentation before submission, or steering you away from a property that looks mortgageable until the valuer comments otherwise.

The fee question

This is the objection buyers often raise first, and reasonably so. Brokers are not free in every case. Some are paid by the lender, some charge the client, and some operate on a mixture depending on case complexity.

The important point is not whether a fee exists. It is whether the fee buys a better outcome, lower total cost, less risk, and less wasted time. In straightforward cases, a buyer may decide to go direct and keep things simple. In anything more nuanced, the cost of getting it wrong can exceed the broker fee very quickly.

Navigating the Whole of Market How Brokers Unlock More Options

“Whole of market” is one of the most overused phrases in mortgage marketing. Buyers hear it and often assume it means every lender, every product, every outcome. In practice, you need to understand what access the broker has, what types of lender they work with, and how they use that access.

Whole of market versus narrower panels

A tied broker works with one lender. A multi-tied adviser works with a restricted group. A whole-of-market broker can search broadly across lenders, subject to their permissions and operational reach.

That matters because first-time buyer cases do not fail only on income multiples. They fail on details. One lender may dislike overtime unless there is a long track record. Another may accept it comfortably. One may accept gifted deposits from close family only. Another may have a wider policy. One may be stricter on flat construction, lease terms, or service charge profile.

Broader market access gives the broker more room to match the case properly.

Why specialist cases need specialist placement

First time buyer mortgage brokers justify their place most clearly in these situations. Complex cases are rarely impossible. They are usually lender-specific.

Common examples include:

Self-employed applicants: Especially where accounts history is shorter or income is uneven.

Freelancers and contractors: Day-rate income can be assessed very differently across lenders.

Gifted deposits: The source is often acceptable, but the paper trail must be clean.

Minor credit blips: Some lenders can work with historic issues more sensibly than others.

Foreign currency or overseas-linked income: Relevant for returning UK nationals, expats, and international families buying in the UK.

A broker with real market reach can separate lenders who merely advertise flexibility from those that reliably underwrite these cases consistently.

Government schemes and lender criteria do not always align neatly

Government schemes and lender criteria do not always align neatly. Scheme knowledge becomes practical rather than theoretical in these situations. Since the Lifetime ISA launched in 2017, over 500,000 first-time buyers have used it, with brokers advising on 60% of these LISA-funded mortgages. That guidance has been associated with an estimated 12% improvement in approval rates through better alignment between the government bonus and lender affordability models, according to HM Treasury information on the Lifetime ISA.

That statistic reflects a reality brokers see regularly. A scheme may help with deposit formation, but the lender still applies its own affordability rules, documentation standards, and property policy. Shared Ownership has its own layers. So do gifted deposits combined with a LISA. So do purchases involving family support from abroad.

A firm such as Willow Private Finance works in this area by matching borrower profile, scheme rules, and lender criteria across residential and more specialist cases, including buyers whose income or residency position is less straightforward.

Market access only matters if the broker knows how each lender interprets the case.

Your Journey with a Broker A Step-by-Step Guide

Most first-time buyers feel calmer once the process is broken into stages. The uncertainty usually comes from not knowing what happens when, who is waiting on whom, and what could delay matters.

In 2024, the average first-time buyer deposit in the UK was about £50,000, representing roughly 11% of the property value, while the average mortgage size was £226,000, according to the FCA mortgage lending statistics. Those are meaningful sums, and the process deserves structure.

First conversation and fact-find

The first meeting is usually about viability and planning, not pressure. A broker will want to understand income, deposit, monthly commitments, property budget, and any complexities.

You should expect questions about:

Employment and income evidence

Current debts and credit commitments

Deposit source

Expected purchase timing

Type of property you want to buy

At this point, honesty matters more than polish. A small issue disclosed early is manageable. A surprise disclosed late can derail a case.

Budget confirmation and agreement in principle

Once the broker has assessed your position, they can identify realistic borrowing capacity and suitable lenders. If the fit is good, the next step is often an agreement in principle.

This matters for two reasons. It helps you search within a sensible range, and it shows agents and sellers that you are financially prepared.

A good broker will not treat this as a generic box-ticking exercise. They will choose the lender carefully, especially if your case has any features that need protecting.

Offer accepted and full application

After your offer is accepted, the pace changes. Documents need to be current, complete, and consistent.

The broker will usually help submit:

Income documents

Bank statements

Proof of deposit

ID and address verification

Property details

Supporting explanations where needed

This is also when inconsistencies matter most. If your payslips, bank statements, and declared outgoings do not line up, the lender will ask questions.

Underwriting, valuation and mortgage offer

The lender then assesses both you and the property. The underwriter reviews the documents. The valuer reviews the property. Either side can create conditions.

Typical issues include:

Queries about spending patterns

Requests for updated documents

Gifted deposit declarations

Valuation comments affecting loan terms

Lease or title issues raised through legal checks

The broker’s role here is partly technical and partly procedural. They answer lender queries, keep communication clear, and help prevent delays caused by incomplete responses.

Legal work and completion

Once the mortgage offer is issued, your solicitor handles the legal process towards exchange and completion. The broker remains relevant even here, especially if dates move, the lender needs updates, or the solicitor raises something that affects funding.

The final stretch often feels slow because several parties are working at once. A broker helps keep the financing side aligned while legal work catches up.

Key Questions to Ask Your Potential Mortgage Broker

Not all brokers work the same way. Some are excellent at straightforward employed cases, but weaker on nuanced income. Some are highly technical but poor at communication. Some are broad in market reach; others are effectively restricted.

Asking the right questions early helps you tell the difference.

Ask about market access

Start with the obvious one, but ask it properly.

Are you whole of market, and what does that mean in practice for my case?

A strong answer should explain whether the broker can access a broad range of lenders and whether they handle specialist scenarios similar to yours. A vague answer usually means the term is being used loosely.

Ask how they handle complexity

Handling complexity well helps good brokers distinguish themselves.

Try questions such as:

How do you approach cases involving gifted deposits?

How do you place applications for self-employed or freelance applicants?

Have you handled buyers with overseas income or recent job changes?

How do you assess scheme-based purchases such as Shared Ownership or a LISA-backed deposit?

You do not need a dramatic case to justify this question. Even modest complexity benefits from a broker who thinks in lender policy rather than general reassurance.

Ask about fees and timing

Do not dance around this. Ask directly.

What is your fee structure, and when is any fee payable?

A good response should be clear about whether the broker is paid by the lender, the client, or both, and at what stage. Ambiguity here creates mistrust later.

Ask who manages the case day to day

Many buyers assume the person who wins the business also handles the case throughout. That is not always how firms operate.

Useful questions include:

Who will be my main contact after the initial recommendation?

How are updates communicated?

How quickly do you normally respond to lender queries?

Good case management is not glamorous, yet it prevents avoidable stress.

Ask how they protect you from the wrong application

This is one of the most revealing questions.

How do you decide which lender not to approach?

An experienced broker should be able to explain how they filter lenders out based on criteria, property type, income treatment, and underwriting approach, which is often more valuable than hearing who they can approach.

Common Pitfalls for First-Time Buyers and How a Broker Helps Avoid Them

The expensive mistakes usually look small at first: a rushed application, an assumption based on an online calculator, a property chosen before checking whether lenders will like it. First-time buyers rarely get into trouble through lack of effort; they get into trouble through lack of lender-specific context.

Mistaking a calculator result for a lending decision

A calculator can be useful for rough planning. It is not underwriting.

A buyer sees a borrowing figure online, makes offers confidently, then learns the chosen lender treats bonus income, probationary employment, or existing credit more harshly than expected. A broker filters this earlier to set a realistic range based on actual lender policy.

Chasing the lowest rate and ignoring the structure

A cheap-looking product can come with fees, conditions, or repayment restrictions that make it poor value in real life.

Brokers look at total cost and suitability, rather than just a headline number. That matters if you may move, overpay, remortgage early, or need flexibility after the initial period.

Mishandling a gifted deposit

Family help is common. The problem is not usually the gift itself, but poor documentation, unexplained transfers, or a mismatch between what the lender expects and what the file shows.

A broker will usually tell you what evidence is needed before the underwriter asks, which reduces delay and suspicion.

Applying to the wrong lender after a rejection

A rejection often pushes buyers into panic mode. They try another lender quickly, then another, without understanding why the first case failed.

That can make a manageable problem worse. A broker will usually diagnose the original issue, rebuild the case if needed, and redirect it more carefully, rather than repeating the same mistake with a different brand.

The broad point is simple. First-time buyer mortgages are not just financial products. They are credit decisions shaped by criteria, presentation, timing, and property detail. That is why first time buyer mortgage brokers remain valuable, especially when the case is not perfectly vanilla.

📞 Want Help Navigating Today’s Market?

Book a free strategy call with one of our mortgage specialists. We’ll help you find the smartest way forward, whatever rates do next.

Tailored advice for individuals, businesses and professional advisers seeking sophisticated financial solutions.

At Willow Private Finance, we understand that every client has different ambitions, financial circumstances and long-term objectives. Whether you are purchasing property, refinancing existing borrowing, protecting your family or business, or looking to unlock wealth through specialist lending, we build solutions around your individual needs rather than forcing you into standard products.

As an independent, whole-of-market brokerage, we provide access to residential mortgages, buy-to-let finance, bridging loans, development finance, commercial lending, private banking and Lombard lending facilities, alongside a comprehensive range of personal and business protection solutions. Our expertise extends to UK and international clients, high-net-worth individuals, company directors, investors, expatriates and borrowers with complex financial structures.

By combining deep technical expertise with relationships across mainstream lenders, specialist lenders and private banks, we help clients secure funding, structure borrowing efficiently and protect the assets, income and people that matter most. Whatever stage of your financial journey you are at, our team is here to provide clear, strategic advice that delivers confidence and long-term value.

From mortgages and private banking to Lombard lending, business finance and protection planning, Willow Private Finance delivers bespoke solutions for even the most complex financial requirements.

Wesley Ranger is a senior finance professional with over 20 years’ experience in the UK mortgage and specialist lending markets. As a director at Willow Private Finance, he has advised extensively on first-time buyer mortgages, helping individuals navigate the complexities of entering the property market.

His expertise includes lender underwriting criteria, deposit structuring, and affordability assessments, particularly for applicants with limited credit history or non-standard income. Wesley has worked with a wide range of buyers, from those purchasing their first home to clients requiring more complex lending solutions early in their property journey.

He has a detailed understanding of how lenders assess first-time buyer applications, including credit scoring, income verification, and government scheme considerations. His experience spans both high street and specialist lenders, providing a comprehensive, whole-of-market perspective.

Wesley regularly advises on structuring mortgage applications to align with lender expectations, ensuring that first-time buyers approach the market with a clear and informed strategy.

Important Notice

This article is for general information purposes only and does not constitute personal financial advice, tax advice, or legal advice. Mortgage availability, criteria, and rates depend on individual circumstances and may change at any time.

Mortgage advice for first-time buyers involves assessing affordability, deposit requirements, credit profile, and lender criteria. Not all borrowers will be eligible for the same terms, and different brokers may have varying levels of lender access and regulatory permissions.

Examples, scenarios, and market commentary are illustrative only and do not represent a guarantee of outcome. First-time buyers should carefully consider their financial position and seek appropriate advice before entering into a mortgage agreement.

Your home may be repossessed if you do not keep up repayments on a mortgage or any debt secured against it.

Willow Private Finance Ltd is authorised and regulated by the Financial Conduct Authority (FCA No. 588422). Registered in England and Wales.

HSBC's reported pullback from parts of the private credit market highlights why developers, family offices and complex borrowers need specialist funding advice.

Gulf buyers from the UAE, Saudi Arabia and Qatar are returning to London's prime property market. Discover why early finance preparation is becoming increasingly important.

Family offices are increasingly outsourcing specialist expertise as portfolios become more complex. Discover why specialist property finance partners are becoming essential for wealth managers, trustees and private client advisers.

Knight Frank's latest research examines how rental reform and future tax risks are reshaping the prime rental market and why landlords should review their finance strategy.

Discover what the Bank of England's 2026 Financial Stability Report means for high-value borrowers, refinancing, private banking and specialist property finance.

New concerns over mansion tax valuations mean owners of £2m+ homes should review property finance, Lombard lending and wealth planning before the High Value Council Tax Surcharge begins in 2028.

NatWest has completed its £2.7bn acquisition of Evelyn Partners, creating the UK's largest private banking and wealth management business. Discover why specialist property finance partnerships matter more than ever.

Financial Times reports growing use of Lombard lending for property purchases as affluent investors borrow against portfolios instead of selling assets.